What is total risk formula

Victoria Simmons

Published Apr 05, 2026

Total risk = Systematic risk + Unsystematic risk Some stocks will go up in value because of positive company-specific events, while. Others will go down in value because of negative company-specific events.

What is total risk in investment?

Total risk is the combination of all risk factors associated with making some type of investment decision. … Both systematic and unsystematic risk, also known as systemic and unsystemic risk, must be considered in order for the total risk to be assessed.

What are the 3 parts of total risk?

- diversifiable risk.

- unique risk.

- company-specific risk.

What is total risk of a stock?

Systematic risk, or total market risk, is the volatility that affects the entire stock market across many industries, stocks, and asset classes. … Unlike with unsystematic risk, diversification cannot help to smooth systematic risk, because it affects a wide range of assets and securities.How do I get a VAR?

- Historical Method. The historical method simply re-organizes actual historical returns, putting them in order from worst to best. …

- The Variance-Covariance Method. …

- Monte Carlo Simulation.

What are the two components of total risk?

- Financial risks. These are risks that are faces a business as a result of using debt sources of finances.

- Business risks. These are risks that result in adverse variation of company’s profit due to factors that may be within or outside management control.

How do you calculate total risk of a stock?

Remember, to calculate risk/reward, you divide your net profit (the reward) by the price of your maximum risk. Using the XYZ example above, if your stock went up to $29 per share, you would make $4 for each of your 20 shares for a total of $80. You paid $500 for it, so you would divide 80 by 500 which gives you 0.16.

Can betas be negative?

Negative beta: A beta less than 0, which would indicate an inverse relation to the market, is possible but highly unlikely. Some investors argue that gold and gold stocks should have negative betas because they tend to do better when the stock market declines.How do you quantify risks?

An expected value can be calculated for each significant risk by multiplying the likelihood of the risk occurring (probability) by the size of the consequence. This risk premium is expressed in monetary terms and provides an estimate of the cost of accepting all the risk.

What is beta a measure of?Beta is a measure of the volatility—or systematic risk—of a security or portfolio compared to the market as a whole. Beta is used in the capital asset pricing model (CAPM), which describes the relationship between systematic risk and expected return for assets (usually stocks).

Article first time published onWhat are the components of the total systematic risk?

Systematic risk is that part of the total risk that is caused by factors beyond the control of a specific company, such as economic, political, and social factors. It can be captured by the sensitivity of a security’s return with respect to the overall market return.

What is a beta value?

Definition: Beta is a numeric value that measures the fluctuations of a stock to changes in the overall stock market. Description: Beta measures the responsiveness of a stock’s price to changes in the overall stock market.

What is VAR in coding?

The var statement declares a variable. Variables are containers for storing information. Creating a variable in JavaScript is called “declaring” a variable: var carName; After the declaration, the variable is empty (it has no value).

What is VAR model in econometrics?

Vector autoregression (VAR) is a statistical model used to capture the relationship between multiple quantities as they change over time. … VAR models generalize the single-variable (univariate) autoregressive model by allowing for multivariate time series. VAR models are often used in economics and the natural sciences.

What is var type in Java?

In Java 10, the var keyword allows local variable type inference, which means the type for the local variable will be inferred by the compiler, so you don’t need to declare that. … Each statement containing the var keyword has a static type which is the declared type of value.

How much should you risk per trade?

Risk per trade should always be a small percentage of your total capital. A good starting percentage could be 2% of your available trading capital. So, for example, if you have $5000 in your account, the maximum loss allowable should be no more than 2%. With these parameters your maximum loss would be $100 per trade.

What is a good risk/reward ratio Crypto?

Again, most analysts advise a risk/reward ratio of no greater than 1:2, or 0.5, for recommended trades.

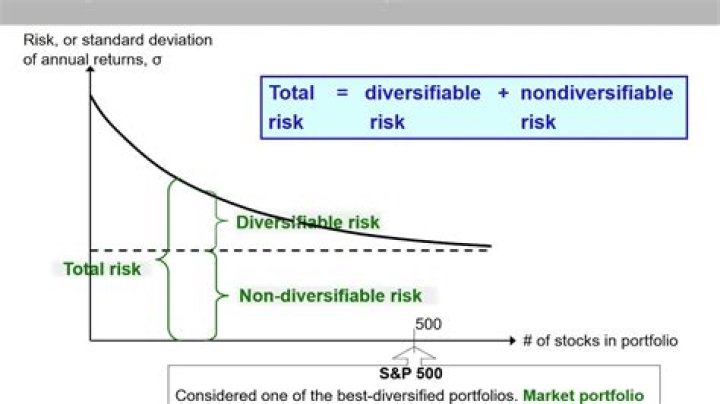

What is total risk of a portfolio?

The portfolio’s total risk (as measured by the standard deviation of returns) consists of unsystematic and systematic risk. … The only risk affecting a well-diversified portfolio is therefore systematic. As a result, an investor who holds a well-diversified portfolio will only require a return for systematic risk.

Is Variance Total risk?

Risk Of Individual Assets Vs. The appropriate measure of the incremental risk of an investment differs from the variance, which is a measure of the total risk of the investment.

How many risk assessment stages are there?

Risk Assessment and the 5 stages. Risk Assessment are carried out in a standard 5 stages. The HSE has a simple process to follow on risk assessing called the 5 steps of a risk assessment.

What is quantified risk model?

Definition. Quantitative Risk Model denotes any quantitative (mathematical) tool that aims to produce systematic risk assessments / estimates for the purpose of Risk Management.

How is business quantified risk?

Business Decisions A formula for measuring business risks is the opportunity cost formula. Opportunity cost = cost of first choice – cost of second alternative. Opportunity cost represents the value or cost of a business activity calculated in relationship to the value of a second alternative.

What is qualify risk?

PMI calls this process Qualitative Risk Analysis. … They say that, “it is the process of prioritizing risks for further analysis or action by assessing and combining their probability of occurrence and impact.”1 Let’s just call it risk prioritization and be done with it.

What does a beta of 2.5 mean?

Beta, also known as the beta coefficient, measures how the expected return of a stock is correlated to the performance of the stock market as a whole. … A positive beta, such as a one or two, means that the stock usually tracks the market in general.

Is High beta good or bad?

What Is Beta? Beta is a measure of a stock’s volatility in relation to the overall market. … High-beta stocks are supposed to be riskier but provide higher return potential; low-beta stocks pose less risk but also lower returns.

Does gold have a beta?

Abstract. Gold shows the characteristics of a zero-beta asset. It has approximately the same mean return as a Treasury Bill and bears no market risk.

What is VAR and how is it calculated?

Incremental Value at Risk Incremental VaR is calculated by taking into consideration the portfolio’s standard deviation and rate of return, and the individual investment’s rate of return and portfolio share. (The portfolio share refers to what percentage of the portfolio the individual investment represents.)

What does a beta of 0 mean?

A zero-beta portfolio is a portfolio constructed to have zero systematic risk, or in other words, a beta of zero. … Such a portfolio would have zero correlation with market movements, given that its expected return equals the risk-free rate or a relatively low rate of return compared to higher-beta portfolios.

What is traded risk?

In the context of trading, risk is the potential that your chosen investments may fail to deliver your anticipated outcome. That could mean getting lower returns than expected, or losing your original investment – and in certain forms of trading, it can even mean a loss that exceeds your deposit.

What is beta in CAPM formula?

The beta (denoted as “Ba” in the CAPM formula) is a measure of a stock’s risk (volatility of returns) reflected by measuring the fluctuation of its price changes relative to the overall market. In other words, it is the stock’s sensitivity to market risk.

What is the difference between systematic and systemic risk?

Systemic risk describes an event that can spark a major collapse in a specific industry or the broader economy. … Systematic risk is the overall, day-to-day, ongoing risk that can be caused by a combination of factors, including the economy, interest rates, geopolitical issues, corporate health, and other factors.