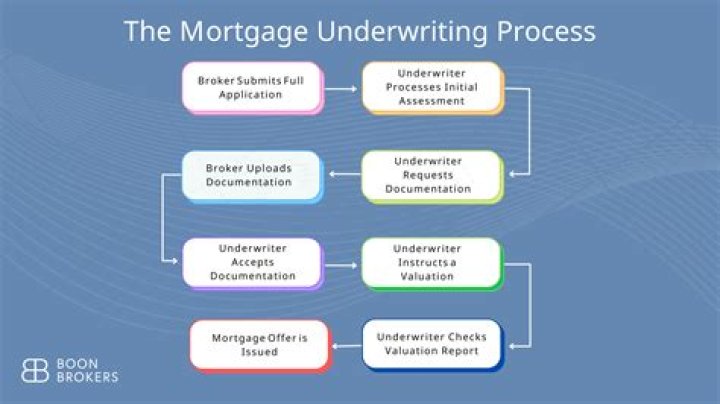

What is the underwriting stage of a mortgage

Victoria Simmons

Published May 26, 2026

Mortgage underwriting is when your lender reviews your home loan application and assesses how risky it would be to lend you money. Before approving your application, your lender has to determine your creditworthiness and the likelihood that you’ll be able to pay back your loan.

How long does it take for the underwriter to make a decision?

Under normal circumstances, initial underwriting approval happens within 72 hours of submitting your full loan file. In extreme scenarios, this process could take as long as a month. However, it’s unlikely to take so long unless you have an exceptionally complicated loan file.

Is underwriting the last step?

No, underwriting is not the final step in the mortgage process. You still have to attend closing to sign a bunch of paperwork, and then the loan has to be funded. … The underwriter might request additional information, such as banking documents or letters of explanation (LOE).

What happens in the underwriting stage of a mortgage?

Underwriting simply means that your lender verifies your income, assets, debt and property details in order to issue final approval for your loan. An underwriter is a financial expert who takes a look at your finances and assesses how much risk a lender will take on if they decide to give you a loan.How long does it take an underwriter to approve a mortgage loan?

Underwriting—the process by which mortgage lenders verify your assets, and check your credit scores and tax returns before you get a home loan—can take as little as two to three days. Typically, though, it takes over a week for a loan officer or lender to complete.

Is no news good news in underwriting?

When it comes to mortgage lending, no news isn’t necessarily good news. … Particularly in today’s economic climate, many lenders are struggling to meet closing deadlines, but don’t readily offer up that information.

How do you know when your mortgage loan is approved?

How do you know when your mortgage loan is approved? Typically, your loan officer will call or email you once your loan is approved. Sometimes, your loan processor will pass along the good news.

What comes after underwriting?

Once your loan goes through underwriting, you’ll either receive final approval and be clear to close, be required to provide more information (this is referred to as “decision pending”), or your loan application may be denied.How long after underwriting is closing?

Clear To Close: At Least 3 Days Once the underwriter has determined that your loan is fit for approval, you’ll be cleared to close. At this point, you’ll receive a Closing Disclosure.

Do underwriters look at spending habits?Banks check your credit report for outstanding debts, including loans and credit cards and tally up the monthly payments. … Bank underwriters check these monthly expenses and draw conclusions about your spending habits.

Article first time published onDoes underwriting happen before or after appraisal?

Mortgage underwriting is usually the next stage that occurs, once the appraiser has completed his or her report. The mortgage lender’s underwriter will review the loan file to make sure all required documents are present.

How many days before closing do you get clear to close?

Cleared to Close (3 days) Getting the all clear to close is the last step before your final loan documents can be drawn up and delivered to you for signing and notarizing. A final Closing Disclosure detailing all of the loan terms, costs and other details will be prepared by your lender and provided to you for review.

Can my loan be denied at closing?

Though it’s rare, a mortgage can be denied after the borrower signs the closing papers. For example, in some states, the bank can fund the loan after the borrower closes. … During this time frame, borrowers have the right to back out of the loan, so the bank may hold off on wiring the money right away.

How often is a loan denied in underwriting?

One in every 10 applications to buy a new house — and a quarter of refinancing applications — get denied, according to 2018 data from the Consumer Financial Protection Bureau.

Does underwriter work on weekends?

It depends on the work load and the company. Working weekends is required sometimes. A smaller company or broker may be more inclined to underwrite on weekends.

Why would an underwriter deny a loan?

Underwriters can deny your loan application for several reasons, from minor to major. … Some of these problems that might arise and have your underwriting denied are insufficient cash reserves, a low credit score, or high debt ratios.

What happens after final approval from underwriter?

After you receive final mortgage approval, you‘ll attend the loan closing (signing). … If this happens, your home loan application could be denied, even after signing documents. In this way, a final loan approval isn’t exactly final. It could still be revoked.

Why would a mortgage be declined?

One of the most common and avoidable reasons for a declined mortgage application is where an error has been made, i.e. incorrect information has caused your application to be declined. Something as simple as a wrong house number on the address, or other small but significant details could result in not being approved.

What is conditional approval after underwriting?

What Does Conditionally Approved Mean? Conditional loan approval means that your mortgage underwriter is mostly satisfied with your mortgage application. … Instead, it means the lender is willing to loan you a specific amount of money if you can meet certain criteria.

Why is underwriter taking so long?

Underwriters often request additional documents. This is when the mortgage lender’s underwriter (or underwriting department) reviews all paperwork relating to the loan, the borrower, and the property being purchased. … It’s another reason why mortgage lenders take so long to approve loans.

What happens if your financing falls through?

The buyer must be able to obtain a mortgage for the property, usually within a specific period of time of signing the contract. Sometimes a condition can be written into the contract whereby if the financing falls through, the contract is nullified.

What happens the week before closing on a house?

1 week out: Gather and prepare all the documentation, paperwork, and funds you’ll need for your loan closing. You’ll need to bring the funds to cover your down payment , closing costs and escrow items, typically in the form of a certified/cashier’s check or a wire transfer.

Is closing Disclosure final approval?

The Closing Disclosure is a final accounting of your loan’s interest rate and fees, mortgage closing costs, your monthly mortgage payment and the grand total of all payments and finance charges. The form is issued at least three days before you sign the mortgage documents.

How far back do mortgage underwriters look?

Mortgage underwriters want to see on-time payment history and re-established credit in the past 12 months.

How close do Underwriters look at bank statements?

How far back do lenders look at bank statements? Lenders typically look at 2 months of recent bank statements along with your mortgage application. You need to provide bank statements for any accounts holding funds you’ll use to qualify for the loan.

Can underwriters see payday loans?

Quite simply, this means that lenders will not see short-term small-dollar loans (payday loans), auto loans through buy here/pay here dealers, even transactions by other installment lenders. …

What are the steps in the underwriting process?

- Step 1: Complete your mortgage application. The first step is to fill out a loan application. …

- Step 2: Be patient with the review process. …

- Step 3: Get an appraisal. …

- Step 4: Protect your investment. …

- Step 5: The underwriter will make an informed decision. …

- Step 6: Close with confidence.

Can loan be denied after appraisal?

The Appraisal Is Too Low A lender cannot lend more than the appraised value of the home. If the appraisal value comes back lower than the sale price, you’ll either need to pay the difference out of pocket or renegotiate to a lower price. If you can’t do either, your loan will be denied.

Why are appraisals taking so long 2021?

If your appraisal is taking a long time in 2021, a combination of factors is likely contributing to the wait. One major issue is that there is a logjam for lenders: Banks are currently working through a ton of mortgage applications as home buyers look to close on new homes, as well as refinancing applications.

How long after closing on a house can you move in?

The contract terms will determine when you can move in after closing. In some cases, it will be immediately after the closing appointment. You will receive the keys and head straight to your new home. In other situations, the seller may request 30, 45 or even 60 days of occupancy after the closing of the home.

Can a closing date be moved up?

Closing dates can be flexible, depending on the parties involved and the required timeline. It is not unusual for a closing date to change, especially if the buyer is financing their purchase, as their loan process must be finalized and all funds in place before closing is possible.