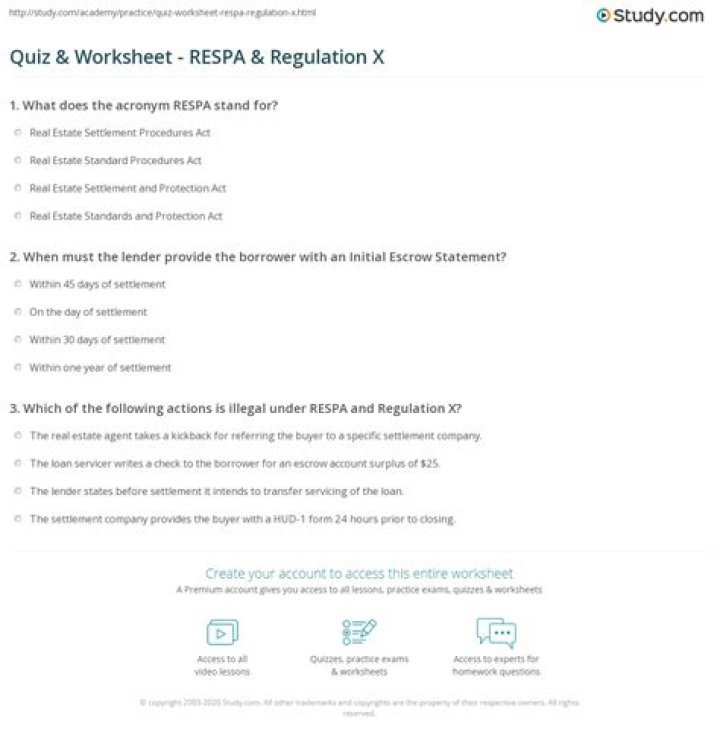

What is respa Regulation X

Robert Spencer

Published Mar 20, 2026

The Act requires lenders, mortgage brokers, or servicers of home loans to provide borrowers with pertinent and timely disclosures regarding the nature and costs of the real estate settlement process. The Act also prohibits specific practices, such as kickbacks, and places limitations upon the use of escrow accounts.

What is Regulation X?

What Is Regulation X? Regulation X is a rule, issued by the Board of Governors of the Federal Reserve System (FRS), that governs credit limits granted to foreign persons or organizations for the purchases of U.S. Treasuries, like T-bonds.

What is Regulation X and Z?

Updated: December 2021. Regulations X and Z have been used to implement the Real Estate Settlement Procedures Act and the Truth in Lending Act for decades. In 2010, the Dodd-Frank Act amended those rules, specifically the rules on the servicers’ obligations.

What does Regulation X apply to?

Regulation X, or “RESPA”, applies to all federally related mortgage loans with few exceptions. RESPA requires specific disclosures and procedures in connection with the application, settlement, and servicing of 1-4 dwelling secured consumer loans.What is regulated by RESPA?

RESPA applies to the majority of purchase loans, refinances, property improvement loans, and equity lines of credit. RESPA requires lenders, mortgage brokers, or servicers of home loans to provide disclosures to borrowers concerning real estate transactions, settlement services, and consumer protection laws.

Does RESPA apply to HELOCs?

The TILA-RESPA rule applies to most closed-end consumer credit transactions secured by real property, but does not apply to: HELOCs; • Reverse mortgages; or • Chattel-dwelling loans, such as loans secured by a mobile home or by a dwelling that is not attached to real property (i.e., land).

What is a RESPA violation?

A RESPA violation occurs when a title company has a financial interest (or ownership) in a real estate transaction where a buyer’s loan is “federally insured.” RESPA is a consumer protection law created to make sure that buyers of residential properties of one to four family units are informed in detailed writing …

Who protects respa?

RESPA covers loans secured with a mortgage placed on one-to-four family residential properties. Originally enforced by the U.S. Department of Housing & Urban Development (HUD), RESPA enforcement responsibilities were assumed by the Consumer Financial Protection Bureau (CFPB) when it was created in 2011.Is Regulation Z part of Tila?

The Truth in Lending Act (TILA) is implemented by the Board’s Regulation Z (12 CFR Part 226). A principal purpose of TILA is to promote the informed use of consumer credit by requiring disclosures about its terms and cost. TILA also includes substantive protections.

Does RESPA apply to FHA?Under RESPA, new rules require lenders to provide specific information on all costs associated with an FHA mortgage, conventional loan or other home loan products. … RESPA forces lenders to give FHA mortgage applicants and other borrowers something called a Good Faith Estimate.

Article first time published onWhat are the RESPA disclosures?

RESPA requires that borrowers receive disclosures at various times in the transaction process. Some disclosures spell out the costs associated with the settlement, outline lender servicing and escrow account practices and describe business relationships between settlement service providers.

What are examples of RESPA violations?

- Giving (non-monetary) gifts in exchange for referrals. …

- Inflating the cost of services. …

- Overcharging for common fees. …

- Paying referral fees to an insurance company. …

- Setting up shell entities to cover up kickbacks.

What is a kickback in RESPA?

RESPA Section 8(a) prohibits the giving and accepting of kickbacks (e.g., cash or other “things of value” as defined in RESPA and Regulation X) pursuant to any agreement or understanding to refer settlement service business or business incident to a real estate settlement service in connection with those loans.

What are considered settlement services under RESPA?

A settlement service includes any service provided in connection with a real estate settlement including, but not limited to, title searches, title examinations, the provision of title certificates, title insurance, services rendered by an attorney, the preparation of documents, property surveys, the rendering of …

What is exempt from RESPA?

The following transactions are exempt from RESPA: • A loan on property of twenty-five acres or more. (whether or not a dwelling is located on the. property) • A loan primarily for business, commercial, or.

Does RESPA apply to condos?

Loans secured by a condominium unit or a cooperative share are covered under RESPA as long as the units are not used for business purposes. … Such a sale is exempt from RESPA coverage as a secondary market transaction.”

What are the 6 pieces of information for Trid?

The six items are the consumer’s name, income and social security number (to obtain a credit report), the property’s address, an estimate of property’s value and the loan amount sought.

What triggers Regulation Z?

Payment information in an advertisement is also a triggering term requiring additional disclosures. … Regulation Z prohibits misleading terms in open-end credit advertisements.

What are the two most important disclosures that appear on the Reg Z disclosure statement?

Reg Z requires disclosure of the finance charge and Annual Percentage Rate (APR) regardless of whether you are granting a revolving credit line or an installment loan. days after approval to give the applicant time to decide whether or not to accept.

What does PITI stand for?

PITI is an acronym that stands for principal, interest, taxes and insurance. Many mortgage lenders estimate PITI for you before they decide whether you qualify for a mortgage.

What is the difference between RESPA and Tila?

TILA is the Truth in Lending Act and RESPA is the Real Estate Settlement Procedures Act.

What is Trid?

“TRID” is an acronym that some people use to refer to the TILA RESPA Integrated Disclosure rule. This rule is also known as the Know Before You Owe mortgage disclosure rule and is part of our Know Before You Owe mortgage initiative.

What does Section 8 of RESPA prohibit?

RESPA Section 8(a) prohibits the giving and accepting of kickbacks (e.g., cash or other “things of value” as defined in RESPA and Regulation X) pursuant to any agreement or understanding to refer settlement service business or business incident to a real estate settlement service in connection with those loans.

Does RESPA Section 8 apply to Helocs?

RESPA uses “federally related mortgage loan” for purposes of section 8 violations. … RESPA certainly does apply to HELOC’s but each disclosure is exempted.

Does RESPA apply to private lenders?

Q. Do the integrated mortgage disclosures apply to private/seller financing and/or land contracts? A. … RESPA still applies to those loans if they qualify as federally related mortgage loans under Regulation X.

What type of loan is not covered by RESPA?

Commercial or Business Loans Normally, loans secured by real estate for a business or agricultural purpose are not covered by RESPA. However, if the loan is made to an individual entity to purchase or improve a rental property of 1 to 4 residential units, then it is regulated by RESPA.

What is the 3 day Trid rule?

Quick Review of the Three Day Closing Disclosure Rule The federal law that regulates the mortgage process (known as the TRID) requires that lenders provide borrowers with a closing disclosure at least three business days before the close of the mortgage.

What is the TILA respa integrated disclosure rule?

TRID is a series of guidelines enforced by the Consumer Financial Protection Bureau (CFPB) that attempt to close some of the loopholes that unscrupulous lenders have used in the past to trick consumers. TRID rules dictate what mortgage information lenders need to provide to borrowers and when they must provide it.

What types of fees and conditions are prohibited under RESPA?

Section 8 of RESPA prohibits anyone from giving or accepting a fee, kickback or anything of value in exchange for referrals of settlement service business involving a federally related mortgage loan. In addition, RESPA prohibits fee splitting and receiving unearned fees for services not actually performed.

Which would not be considered a RESPA violation?

Which would NOT be considered a RESPA violation? A thing of minimal value used in the course of sales such as pens, mementos, coffee cups, hats, etc. is permissible, but the other three arrangements could be considered violations of RESPA. To violate RESPA, the thing of value does not have to be money.