What is relevant cash flow

Emily Dawson

Published Mar 20, 2026

Definition. A definition often used for relevant cash flows states that they must be cash flows that occur in the future and are incremental. … Any relevant cash flow should arise in the future. Anything that has occurred in the past is referred to as a sunk cost and should be excluded from relevant cash flows.

What is a relevant cash flow in capital budgeting?

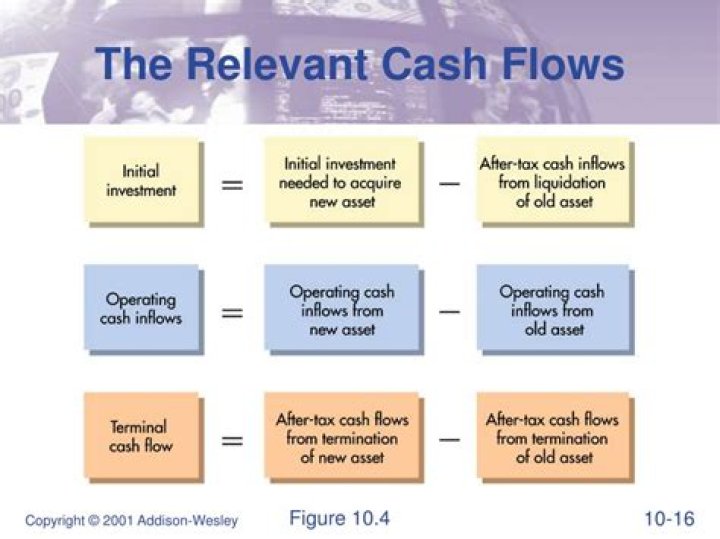

All relevant cash flows for a project must be included in the capital budgeting analysis for a project. Relevant cash flows are those that change as a result of accepting the project.

Is a relevant cost a cash flow?

Definition of Relevant Costs The relevant cash flows are future, incremental cash flows arising from the decision being made. This means that the cash flows are only relevant if they are future, incremental costs. Relevant costs are used for taking an investment decision.

What is non relevant cash flow?

Non relevant costs Non cash flow costs are costs which do not involve the flow of cash, for example, depreciation and notional costs.What are the 4 types of cash flows?

Cash flow analysis first requires that a company generate cash statements about operating cash flow, investing cash flow and financing cash flow.

What is terminal cash flow?

Terminal cash flows are cash flows at the end of the project, after all taxes are deducted. In other words, terminal cash flows are the net amount made by company after disposing the asset and necessary amounts are paid.

How do we determine if cash flows are relevant to the capital budgeting decision?

The capital budgeting process will usually examine a project’s cash flows to determine whether the project is feasible for new investment. Generally, if cash inflows exceed the cash outflows, considering the time value of money, the project should be accepted.

What is a relevant cost in accounting?

‘Relevant costs’ can be defined as any cost relevant to a decision. A matter is relevant if there is a change in cash flow that is caused by the decision. The change in cash flow can be: additional amounts that must be paid. a decrease in amounts that must be paid.What is relevant cost example?

Relevant cost is a managerial accounting term that describes avoidable costs that are incurred only when making specific business decisions. … As an example, relevant cost is used to determine whether to sell or keep a business unit.

What is the difference between relevant and irrelevant cost?Relevant costs are costs that will be affected by a managerial decision. Irrelevant costs are those that will not change in the future when you make one decision versus another. Examples of irrelevant costs are sunk costs, committed costs, or overheads as these cannot be avoided.

Article first time published onIs working capital a relevant cash flow?

If working capital increases year over year, the company has tied up more cash in working capital. … Accordingly, cash flow decreases as accounts receivables increase or accounts payables decrease. Therefore, as working capital changes from period to period, it has an effect on cash flow, which in turn affects NPV.

What is relevant revenue?

(also called relevant revenues and costs or incremental revenues and costs) represent the difference in revenues and costs among alternative courses of action. … Alternative 1 includes the annual revenues, costs, and resulting profit if the company keeps all existing customers.

What is relevant cost PDF?

Relevant cost – Cost that should be used in decision making is called as relevant cost. … Sunk cost: These are the cost incurred in the past and cannot be affected by a future decision. Sunk cost is therefore, irrelevant cost for decision making. Eg Development cost which has been already incurred. 2.

How many types of cash flows are there?

The three types of cash flows are operating cash flows, cash flows from investments, and cash flows from financing.

What are the methods of cash flow?

There are two ways to prepare a cash flow statement: the direct method and the indirect method: Direct method – Operating cash flows are presented as a list of ingoing and outgoing cash flows. Essentially, the direct method subtracts the money you spend from the money you receive.

What are the three activities of cash flow statement?

The cash flow statement is the least important financial statement but is also the most transparent. The cash flow statement is broken down into three categories: Operating activities, investment activities, and financing activities.

What are the three types of risk that are relevant in capital budgeting?

The three types of risk in capital budgeting are Stand-alone risk, Corporate risk, and Market risk.

Why cash flows are preferred over accounting profits in capital expenditure decisions?

1-We focus on cash flows rather than accounting profits in making our capital budgeting decisions because earnings include non-cash transactions like depreciation and credit sales. 2-Our goal is to compare business projects, not total cash flow, which is why we care about incremental cash flows.

Why are cash flows used in NPV?

NPV uses discounted cash flows due to the time value of money (TMV). The time value of money is the concept that money you have now is worth more than the identical sum in the future due to its potential earning capacity through investment and other factors such as inflation expectations.

What is the formula for terminal cash flow?

Terminal value is calculated by dividing the last cash flow forecast by the difference between the discount rate and terminal growth rate. The terminal value calculation estimates the value of the company after the forecast period. Where: FCF = free cash flow for the last forecast period.

How do you calculate DCF?

- DCF Formula =CFt /( 1 +r)t

- TVn= CFn (1+g)/( WACC-g)

- FCFF=Net income after tax+ Interest * (1-tax r. …

- WACC=Ke*(1-DR) + Kd*DR.

- Ke=Rf + β * (Rm-Rf)

- FCFE=FCFF-Interest * (1-tax rate)-Net repayments of debt.

Can Terminal cash flow be negative?

Yes it can be negative! This might theoretically be possible if you use the perpetuity growth method to calculate terminal value. If you refer to the formula, this is derived when the free cashflow growth rates exceed the cost of capital.

What is relevant range accounting?

The relevant range refers to a specific activity level that is bounded by a minimum and maximum amount. Within the designated boundaries, certain revenue or expense levels can be expected to occur. Outside of that relevant range, revenues and expenses will likely differ from the expected amount.

What are the two types of relevant cost?

The types of relevant costs are incremental costs, avoidable costs, opportunity costs, etc.; while the types of irrelevant costs are committed costs, sunk costs, non-cash expenses, overhead costs, etc.

What is another term for relevant costs?

Definition: Relevant cost, also called differential cost, is a management accounting term decsribing costs that pertain to a particular decision.

Why opportunity cost is a relevant cost?

Relevant costs may also be expressed as opportunity costs. An opportunity cost is the benefit foregone by choosing one opportunity instead of the next best alternative. b) of selling it if a buyer could be found (the proceeds are unlikely to exceed $800). … This total is a true representation of ‘economic cost’.

What are the two properties of a relevant cost?

Characteristics of Relevant Costs Two important characteristic features of relevant costs are ‘Occurrence in Future’ and ‘Different for Different Alternatives’. This does not mean that all costs which occur in future are not relevant cost.

Is direct labor a relevant cost?

In this example, which costs are relevant costs? The raw material price and the direct labor cost both make a difference, so both of these costs would be relevant as you looked at your options. … Then the direct labor cost would be come in irrelevant cost.

What are relevant revenues and relevant costs for decision making?

In cost accounting, relevant means that you consider future revenue and expenses. Also, relevant means that a cost or revenue will change, depending on a decision you make. Past costs are water under the bridge, and if the costs or revenue remain the same no matter what you decide, they aren’t relevant.

What is relevant and irrelevant information?

Relevant information would include changes in temperature, winds, and rainfall. Information that is irrelevant to this topic would include changes in government or cultural traditions.

Is salvage value a relevant cost?

Salvage value is defined as “The estimated value of an asset at the end of its useful life.” … It is often said in economics that “sunk costs are sunk”, meaning they should not be considered a cost in economic analysis, because the money has already been spent.