What is an insured escrow

Christopher Lucas

Published Mar 02, 2026

If you’ve ever wondered, “what is insurance escrow,” it’s simply an account managed by a third party. When buying a house, an escrow home insurance account will be opened, incurring a number of fees that aren’t owed to your lender, but that need to be paid in order to keep up with your house.

What is insured escrow HUD home?

When you buy a fixer-upper from HUD, you may qualify for a special loan from the FHA that allows you to borrow enough money to both buy the property and repair it. The HUD repair escrow is an escrow account where the funds for repairs are held until the work is completed.

How does FHA repair escrow work?

An FHA repair escrow allows a borrower to purchase a home that needs repairs using a mortgage. Lenders typically will not issue a loan for a home that includes funds for repairs.

What is a FHA 203k loan with escrow repair?

The 203(b) with Repair Escrow allows homebuyers to finance up to 96.5% of the purchase of a HUD home, as well as necessary and qualified home improvements, using the same mortgage loan. The repair funds are put into a separate account and used as needed while the work is completed.Should I pay insurance through escrow?

No, you don’t have to pay your homeowners insurance through escrow. However, if you’re going to carry a loan on your home and still owe money to the lender, many lenders will require you to have an escrow account set up.

Can you do an escrow holdback on a FHA loan?

The FHA escrow hold-back program helps FHA borrowers finance repair costs as well as fix required repairs after closing. Only FHA appraiser or underwriter required repairs are escrow hold-back eligible. … The FHA buyer and/or the seller is allowed to fund the escrow hold-back.

Does home insurance come out of escrow?

Typically, your escrow payment covers part of your property taxes, mortgage insurance and homeowners insurance. … When your taxes and homeowners insurance fall due, your mortgage lender generally uses the funds in the account to pay those bills on your behalf.

What is FHA IE?

IE – Insured with Escrow Repairs: Properties listed as “INSURED WITH ESCROW REPAIRS” means that certain repairs (not to exceed $5,000.00) are required to meet Minimum Property Standards for an FHA mortgage. Purchasers of these properties have the option to purchase “as-is” with cash or conventional financing.What is the difference between 203k and 203b?

The major difference between an FHA 203(b) and a 203(k) mortgage loan is that one is intended for homes in need of extensive repair while the other one isn’t.

What are the cons of a 203k loan?- Only eligible for primary residences.

- Mortgage Insurance Premium (MIP) required (can be rolled into loan)

- Do it yourself work not allowed*

- More paperwork involved as compared to other loan options.

Is FHA 203k a good idea?

FHA 203k loans are ideal for buyers looking to renovate. You roll all the costs together, only have to deal with single monthly payments and can decide between structural or cosmetic options.

What is the maximum 203k loan amount?

What is the maximum 203k loan amount? You can borrow up to 110 percent of the property’s proposed future value, or the home price plus repair costs, whichever is less.

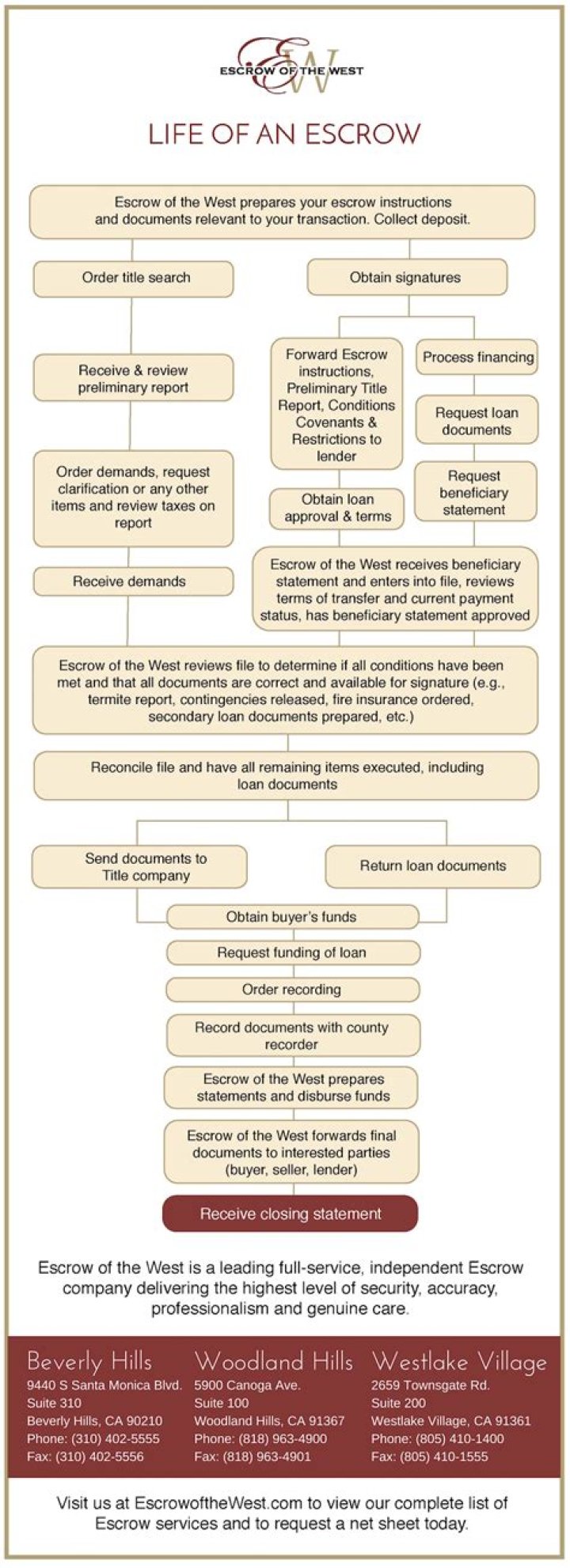

How does escrow work when buying a house?

To protect both the buyer and the seller, an escrow account will be set up to hold the deposit. The good faith deposit will sit in the escrow account until the transaction closes. The cash is then applied to the down payment. Sometimes, funds are held in escrow past the completion of the sale of the home.

What happens after closing escrow?

The earnest money is released from the escrow account and the lender cuts the seller a single big check. Unless the buyer and seller have otherwise negotiated, the buyer takes official possession of the property on the actual date of closing.

Can FHA buyer pay for repairs?

FHA 203k Loan: Buy and Repair A Home with One Loan An FHA 203k loan even allows borrowers to make cosmetic fixes to the home while bringing the home up to FHA minimum standards. This loan program allows up to about $31,000 in repair work with this great loan program.

How can I lower my escrow payment?

- Dispute your property taxes. Call your local assessor if you think your property tax bill is too high, and ask about the process to dispute your bill.

- Shop around for homeowners insurance. …

- Request a cancellation of your private mortgage insurance.

Can I remove escrow from my mortgage?

You must make a written request to your lender or loan servicer to remove an escrow account. Request that your lender send you the form or ask them where to obtain it online, such as the company’s website. The form may be known as an escrow waiver, cancellation or removal request.

How long do you pay escrow?

When you’re in the process of buying a home, you’re “in escrow” between the time that your offer — with its cash deposit — is accepted and the day that you close and take ownership. That’s usually at least 30 days.

Why did I get a check from my home insurance?

Why did you get an insurance refund check in the first place? Because your escrow account had already made insurance premium payments to your old insurance carrier. If you cancel your coverage, your old carrier must provide a prorated refund for those payments to you (subject to policy terms).

Can you pay homeowners insurance separate from mortgage?

If you pay for your homeowners insurance as part of your mortgage, you have an escrow. An escrow is a separate account where your lender will take your payments for homeowners insurance (and sometimes property taxes), which is built into your mortgage, and makes the payments for you.

Do I pay homeowners insurance through mortgage?

However, homeowners insurance is not included in your mortgage. … Your mortgage lender may set up an escrow account3 from which to pay your homeowners insurance and property taxes.

How long must you pay mortgage insurance on a FHA loan?

While the law has changed more than once on this issue, current guidance states that borrowers who put down less than 10 percent on an FHA loan must pay for FHA mortgage insurance until the entire loan term is over. If you put down at least 10 percent, however, you can have FHA MIP removed after 11 years of payments.

Is money held in escrow taxable?

Section 468B(g) states that an escrow account is subject to current income tax. Although the escrow account does not qualify as a designated settlement fund or a qualified settlement fund under 468B(g) that does not preclude current taxation of the interest income.

What is the minimum credit score for maximum financing on a FHA 203b program?

If the credit score is less than 500, then the borrower is not eligible for FHA-insured financing. If the borrower’s credit score is at or above 580, then the borrower is eligible for maximum financing with a loan-to-value ratio (LTV) of 96.5 percent.

Is 203b a renovation loan?

It provides money for the purchase and renovation of a home at the same time. The 203 B loan mentioned in the question, on the other hand, is essentially the FHA standard single family home loan.

What credit score do I need for a 203k loan?

Lenders require applicants to possess a credit score of at least 500. An FHA 203(k) loan requires a minimum down payment of 3.5% for those who possess a credit score of 580 or above, and 10% for those with a lower score.

What is insurability status IE?

IE-Insurable w/escrow: Property eligible for a 203(b) FHA loan; necessary repairs total less than $10,000. … UI-Uninsurable: Property requires more than $10,000 in repairs to meet FHA guidelines and is not eligible for FHA mortgage insurance in the property’s “as is” condition.

How do I qualify for a FHA 203k loan?

Credit score: You’ll need a credit score of at least 500 to qualify for an FHA 203(k) loan, though some lenders may have a higher minimum. Down payment: The minimum down payment for a 203(k) loan is 3.5% if your credit score is 580 or higher. You’ll have to put down 10% if your credit score is between 500 and 579.

What determines FHA 203b residential mortgage loan limits?

Debt-to-income (DTI) ratio of 43% or less, though lenders may accept higher DTI with “significant compensating factors”. Loan amount must be within FHA mortgage limits (limits vary by location and property; current standard mortgage limit for single-family homes is $331,760, or up to $765,600 in high-cost areas).

Do contractors like 203k loans?

But because for the first part of the project the contractor is working “on credit” – meaning they don’t get any money up front to start work or pay for supplies, many contractors don’t like to work with homeowners doing 203k loans, especially since it can be a hassle on their end to get paid.

What does 203k mean in real estate?

Section 203(k) insurance enables homebuyers and homeowners to finance both the purchase (or refinancing) of a house and the cost of its rehabilitation through a single mortgage or to finance the rehabilitation of their existing home.