What is Ac reorganization

Emily Dawson

Published Feb 16, 2026

A C-reorganization, otherwise known as a “practical merger,” is where a target. corporation (“Target”) transfers “substantially all” of its properties to an acquiring. corporation (“Acquiror”) solely in exchange for all or a part of Acquiror’s “voting.

Do you need a business purpose for an F reorganization?

As with any Sec. 368(a) reorganization, the F reorganizations in the examples above must have a valid business purpose and satisfy additional judicial doctrines such as economic substance.

Can AC Corp do an F reorg?

Liquidation of transferor corporation: The transferor corporation must completely liquidate, for federal income tax purposes, in the potential F reorganization; however, the transferor corporation is not required to dissolve under applicable law and may retain a de minimis amount of assets for the sole purpose of …

What is an A reorganization?

In an A reorganization, the target corporation (“Target”) merges into the acquiring corporation (“Acquiring”) with the former Target shareholders receiving the merger consideration in exchange for their Target stock.What is Type B reorganization?

Overview. A Type “B” reorganization is a stock-for-stock transaction in which one corporation (the acquiring corporation) acquires the stock of another corporation (the target corporation). Only voting stock of the acquiring corporation or its parent may be used in the acquisition.

Do disregarded entities file tax returns?

Does a Disregarded Entity Have to File Tax Returns? Since the owner pays the disregarded entity’s federal taxes on their personal return, the disregarded entity is not required to file a federal income tax return.

How does an F reorganization work?

The F Reorganization can facilitate a freeze when you have an existing corporation by creating a two-tier structure where a corporation owns the preferred shares or units of a subsidiary corporation or LLC, and then new common shares or units are issued to new owners/investors in the subsidiary.

How do you reorg?

- Start with your business strategy. …

- Identify strengths and weaknesses in the current organizational structure. …

- Consider your options and design a new structure. …

- Communicate the reorganization.

Is a Subchapter S corporation the same as an S corporation?

An S corporation, also known as an S subchapter, refers to a type of corporation that meets specific Internal Revenue Code requirements. If it does, it may pass income (along with other credits, deductions, and losses) directly to shareholders, without having to pay federal corporate taxes.

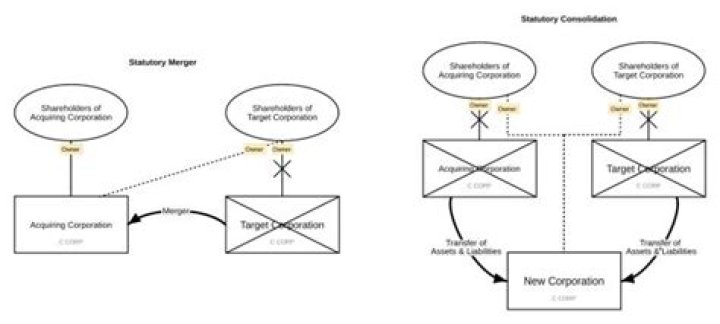

What are the main types of corporate reorganization?- Mergers and consolidations. A statutory merger is based on the acquisition of a company’s assets by another company, either in the same or different industry. …

- Corporate buyouts. …

- Corporate takeovers. …

- Recapitalization. …

- Divestiture (Spinoffs and split-offs)

What is another word for reorganization?

rearrangementrestructuringreshufflereformreformationredeploymentreconstitutionreestablishmentshake-upsort-out

Do you need a new EIN for F reorg?

The previously assigned EIN should be used by the surviving corporation in a statutory merger and in a reincorporation qualifying as an F reorganization. A new EIN should be requested by the new corporation in a consolidation and in any reincorporation transaction not qualifying as an F reorganization.

What is a tax free reorganization?

Certain types of corporate acquisitions, divisions, and other restructurings which are generally not taxable at the corporate or stockholder level. The transaction must meet strict statutory and non-statutory requirements (see IRC § 368 and Treasury Regulations ).

What is a QSub?

A qualified subchapter S subsidiary (QSub) is a subsidiary corporation 100% owned by an S corporation that has made a valid QSub election for the subsidiary (Sec. … The QSub election terminates the QSub’s former identity as a separate entity for federal tax purposes.

What is a section 368 Reorganization?

Internal Revenue Code (IRC) Section 368 allows merger and acquisition transactions to qualify as a reorganization when an acquiring corporation gives a substantial amount of its own stock as consideration to the acquired (or “target”) corporation.

What is a Type B merger?

A Type “B” acquisition has the following characteristics: Cash cannot exceed 20% of the total consideration. At least 80% of the acquiree’s stock must be acquired with the acquirer’s voting stock. The acquirer must buy at least 80% of the acquiree’s outstanding stock.

What is a reverse triangular merger?

What Is a Reverse Triangular Merger? A reverse triangular merger is the formation of a new company that occurs when an acquiring company creates a subsidiary, the subsidiary purchases the target company, and the subsidiary is then absorbed by the target company.

Is an S corporation?

S corporations are corporations that elect to pass corporate income, losses, deductions, and credits through to their shareholders for federal tax purposes. … S corporations are responsible for tax on certain built-in gains and passive income at the entity level.

What is a disregarded entity?

A disregarded entity is a business entity that (1) has a single owner, (2) is not organized as a corporation, and (3) has not elected to be taxed as a separate entity for federal tax purposes. The owner of a disregarded entity reports the income of the disregarded entity on the owner’s return.

How do I report a merger on my taxes?

A reporting corporation must file Form 8806 to report an acquisition of control or a substantial change in the capital structure of a domestic corporation. The reporting corporation or any shareholder is required to recognize gain (if any) under section 367(a) and the related regulations as a result of the transaction.

Does a disregarded entity need an EIN?

Most new single-member LLCs classified as disregarded entities will need to obtain an EIN. … A single-member LLC that is a disregarded entity that does not have employees and does not have an excise tax liability does not need an EIN. It should use the name and TIN of the single member owner for federal tax purposes.

Is a single-member LLC bad?

First, like all LLC’s, a single-member LLC is designed to protect against personal liability. … The disadvantage of a single-member LLC is the risk that, unlike multiple-member LLC’s, it will not protect against personal liability in the event of a lawsuit or other claim.

Are all single member LLCs disregarded entities?

All single-member LLCs are by default considered disregarded entities. This means that the IRS does not treat your LLC as an entity separate from you, its owner, when it comes to income taxes.

Who pays more taxes LLC or S corp?

Tax Liability and Reporting Requirements LLC owners must pay a 15.3% self-employment tax on all net profits*. S corporations have looser tax and filing requirements than C corporations. An S corp. is not subject to corporate income tax and all profits pass through the company.

Is LLC and INC the same?

“LLC” stands for “limited liability company.” The abbreviations “inc.” and “corp.” indicate that a business is a corporation. Both LLCs and corporations are formed by filing forms with the state. Both protect their owners from liability for business obligations.

Which is better an LLC or partnership?

In general, an LLC offers better liability protection and more tax flexibility than a partnership. But the type of business you’re in, the management structure, and your state’s laws may tip the scales toward partnership.

What are some problems associated with frequent reorganization?

- Moving from Strategy to Execution. …

- Talent Gaps and Overlap. …

- Leader Involvement. …

- Employee Communication.

What do you do after reorganization?

- Listen to and absorb what senior leadership says about why the reorg is happening.

- Show compassion for colleagues directly affected.

- Seek opportunities to use your skills and expertise to help your organization through the transition.

What is the difference between a liquidation and a reorganization?

In a reorganization, the debtor retains ownership of its assets and continues business operations while renegotiating debt repayments with creditors. In a liquidation, the creditors seize control of the debtors assets and sell them to pay off the debt. … After liquidation, the entity technically no longer exists.

What is a reorganization in corporate law?

Reorganization is: 1) The implementation of a business plan to alter a corporation’s structure or finances because of financial duress, a desire to change strategy, or a government order. … 2) See Chapter 11 Bankruptcy and Small Business Reorganization Act.

What companies have reorganized?

- Facebook. When Facebook announced its first reorganization in 2011, the reasons included a desire to accommodate growth and streamline the company’s product development process. …

- Tesla. …

- The Wall Street Journal. …

- Hulu. …

- Google. …

- Disney.