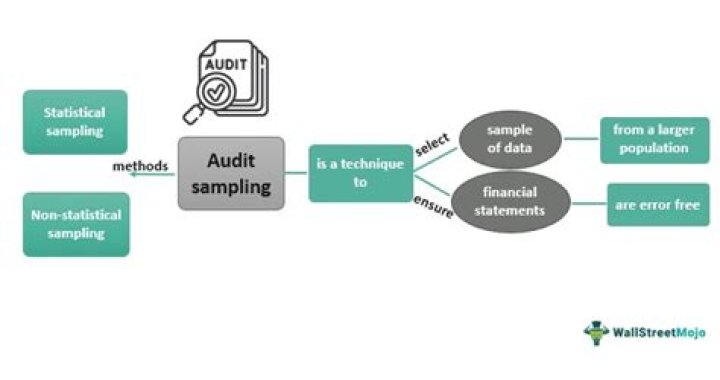

What is a sample in audit

Sophia Edwards

Published Feb 26, 2026

Audit sampling is the use of an audit procedure on a selection of the items within an account balance or class of transactions. The sampling method used should yield an equal probability that each unit in the sample could be selected. The intent behind doing so is to evaluate some aspect of the information.

What is audit sampling and why sample is taken?

Audit sampling enables auditors to make conclusions and express fair opinions based on predetermined objectives without having to check all of the items within financial statements. The auditors will only verify selected items, and through sampling, can infer their opinion on the entire population of items.

When should you increase audit sample size?

1. An increase in the auditor’s assessment of the risk of material misstatement Increase The higher the auditor’s assessment of the risk of material misstatement, the larger the sample size needs to be. The auditor’s assessment of the risk of material misstatement is affected by inherent risk and control risk.

What is sampling unit in audit?

What is a Sampling Unit in Auditing? A sampling unit is a selection of a population that is used as an extrapolation of the population. For example, a household is used as a sampling unit, under the assumption that the polling results from this unit represents the opinions of a larger group.How do you determine a sample size?

- Determine the population size (if known).

- Determine the confidence interval.

- Determine the confidence level.

- Determine the standard deviation (a standard deviation of 0.5 is a safe choice where the figure is unknown)

- Convert the confidence level into a Z-Score.

How do auditors select samples?

The method of sampling is a value-weighted selection whereby sample size, selection and evaluation will result in a conclusion in monetary amounts. … select the sample. perform the audit procedures. evaluate the results and arriving at a conclusion about the population.

What do you mean by sampling?

Sampling is a process used in statistical analysis in which a predetermined number of observations are taken from a larger population. The methodology used to sample from a larger population depends on the type of analysis being performed, but it may include simple random sampling or systematic sampling.

What are the two approaches to audit sampling?

The auditor usually will have no special knowledge about other account balances and transactions that, in his judgment, will need to be tested to fulfill his audit objectives. Audit sampling is especially useful in these cases. . 03 There are two general approaches to audit sampling: nonstatistical and statistical.What are sampling methods?

- Simple random sampling. …

- Systematic sampling. …

- Stratified sampling. …

- Clustered sampling. …

- Convenience sampling. …

- Quota sampling. …

- Judgement (or Purposive) Sampling. …

- Snowball sampling.

An auditor who applies statistical sampling uses tables or formulas to compute sample size based on judgments about factors such as characteristics of the population and certain assessed risks.

Article first time published onWhat is ISI in auditing?

auditor’s professional judgment. Tolerable misstatement is abbreviated as TM; the lower. limit for individually significant items is abbreviated as LL of ISIs.

What meant by sampling risk?

Sampling risk is the risk that the auditor’s conclusions based on a sample may be different from the conclusion if the entire population were the subject of the same audit procedure. … The auditor concludes that controls are operating effectively, when in fact they are not.

What is an example of sample size?

The Definition of Sample Size Sample size measures the number of individual samples measured or observations used in a survey or experiment. For example, if you test 100 samples of soil for evidence of acid rain, your sample size is 100.

What is a good sample size?

A good maximum sample size is usually 10% as long as it does not exceed 1000. A good maximum sample size is usually around 10% of the population, as long as this does not exceed 1000. For example, in a population of 5000, 10% would be 500.

What is considered a small sample size?

Although one researcher’s “small” is another’s large, when I refer to small sample sizes I mean studies that have typically between 5 and 30 users total—a size very common in usability studies. … To put it another way, statistical analysis with small samples is like making astronomical observations with binoculars.

What is sampling and sample?

A sample is a subset of individuals from a larger population. Sampling means selecting the group that you will actually collect data from in your research.

Why do we sample?

Sampling is done because you usually cannot gather data from the entire population. Even in relatively small populations, the data may be needed urgently, and including everyone in the population in your data collection may take too long.

What is audit sampling PDF?

Audit sampling is the application of an audit procedure (test of control or substantive testing) to less than 100% of the items within an account balance or class of transactions for the purpose of drawing a general conclusion about the account balance or the entire group of transactions based on the characteristics …

How do you calculate sampling risk?

The allowance for sampling risk is the level of uncertainty associated with sampling. It is calculated as the difference between the tolerable deviation and the expected mean of the population.

What is sampling error audit?

Sampling error is the difference between the value derived for a population from using a sample and the actual value of the population. … This error can be significant when an auditor does not select a sample that is representative of the entire population.

What is sample size and sampling techniques?

The process of selecting a sample is known as sampling. … Number of elements in the sample is the sample size.

What is sample size in research?

Sample size refers to the number of participants or observations included in a study. … The study’s findings could describe the population of all runners based on the information obtained from the sample of 100 runners.

What are the 4 sampling strategies?

- Random sampling.

- Stratified random sampling.

- Systematic sampling.

- Rational sub-grouping.

What is sampling and its objectives?

One of the frequently asked question is “what is sampling & its objective?” Sampling is the method of collecting the part or portion of data points from the population and ascertaining the population characteristics. Sampled data points are further used for statistical analysis purpose.

Why is statistical sampling important?

Statistical sampling can be a valuable tool to collect and evaluate information about a large population, or universe, when it would otherwise be impractical (or impossible) to collect that information from the entire population.

What is non statistical sampling?

Non-statistical sampling is the selection of a test group that is based on the examiner’s judgment, rather than a formal statistical method. For example, an examiner could use his own judgment to determine one or more of the following: The sample size.

How do I calculate sample size in Excel?

- Enter the observation data in Excel, one observation in each cell. …

- Type “=COUNT(” in cell B1.

- Highlight the cell range of the data or type the cell range of the data after the “(” entered in Step 2 in cell B1, then end the formula with a “)”. …

- references.

What is PSA 320?

PSA 320 (Revised and Redrafted) Introduction. Scope of this PSA. 1. This Philippine Standard on Auditing (PSA) deals with the auditor’s responsibility to apply the concept of materiality in planning and performing an audit of financial statements.

What is threshold in auditing?

The materiality threshold in audits refers to the benchmark used to obtain reasonable assurance that an audit does not detect any material misstatement that can significantly impact the usability of financial statements.

What is rule of thumb in audit?

Auditors make decisions based upon a 5% rule. Misstatements of less than 5% have no effect on financial statement fairness. The 5% rule is widely used in practice.

What is the relationship between sample size and sampling risk?

Sampling risk and non sampling risk The risk can be reduced by increasing sample size. There an inverse relationship between sample size and sampling risk. That is, the greater the sampling size the lower will be the sampling risk. Accordingly, if all items in a population are checked, the sampling risk ill be zero.