What is a RESPA violation

Mia Morrison

Published Mar 02, 2026

A RESPA violation occurs when a title company has a financial interest (or ownership) in a real estate transaction where a buyer’s loan is “federally insured.” RESPA is a consumer protection law created to make sure that buyers of residential properties of one to four family units are informed in detailed writing …

What are examples of RESPA violations?

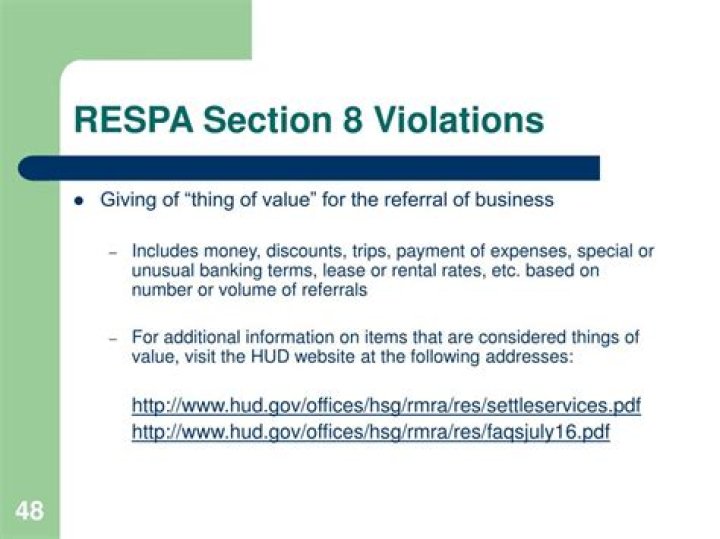

- Giving (non-monetary) gifts in exchange for referrals. …

- Inflating the cost of services. …

- Overcharging for common fees. …

- Paying referral fees to an insurance company. …

- Setting up shell entities to cover up kickbacks.

How should a violation of RESPA be reported?

RESPA Complaints can be submitted confidentially to HUD as well. If you believe you have a potential litigation matter with RESPA to HUD, I would recommend that you submit your complaint to your attorneys prior to submission to the HUD office or let your attorneys file the complaint for you.

Does violation of RESPA include both civil and criminal penalties?

RESPA Section 8 Individuals and businesses that violate Section 8 are subject to both criminal and civil penalties. Criminal penalties can include fines of up to $10,000 and imprisonment up to one year.What is the penalty for a loan officer violating RESPA by paying a referral fee to a real estate agent?

Any person who violates RESPA may be: fined up to $10,000; imprisoned for up to one year; and. held liable for three times the amount paid for the settlement service to the person charged for the settlement service.

Does RESPA allow fee splitting?

RESPA Section 8(b) prohibits the giving and accepting of any portion, split, or percentage of charges made or received for real estate settlement service business, unless for services actually performed.

Which would not be considered a RESPA violation?

Which would NOT be considered a RESPA violation? A thing of minimal value used in the course of sales such as pens, mementos, coffee cups, hats, etc. is permissible, but the other three arrangements could be considered violations of RESPA. To violate RESPA, the thing of value does not have to be money.

Which could result if your institution violates the prohibition against kickbacks?

Rules and regulations that prohibit kickbacks, referrals, and fee splitting, are subject to the most severe penalties for violation of RESPA including fines of up to $10,000 and one year in prison.What are considered settlement services under RESPA?

A settlement service includes any service provided in connection with a real estate settlement including, but not limited to, title searches, title examinations, the provision of title certificates, title insurance, services rendered by an attorney, the preparation of documents, property surveys, the rendering of …

What are the penalties for violating Section 8 of RESPA?Section 8: Kickbacks, Fee-Splitting, Unearned Fees In a criminal case, a person who violates Section 8 may be fined up to $10,000 and imprisoned up to one year.

Article first time published onWhat are RESPA rules?

RESPA prohibits loan servicers from demanding excessively large escrow accounts and restricts sellers from mandating title insurance companies. A plaintiff has up to one year to bring a lawsuit to enforce violations where kickbacks or other improper behavior occurred during the settlement process.

Which of the following would violate Section 8 of RESPA?

To violate the RESPA Section 8(a) prohibition against fees, kickbacks, or things of value and the equivalent Regulation X, Section 3500.14, three elements must be present. First, there must be a payment or giving of a thing of value. Second, the payment must be paramount to an agreement to refer business.

What is a TILA violation?

Some examples of TILA violations include a creditor failing to accurately disclose the APR and finance charge, the misapplication of the daily interest factor, and the application of penalty fees exceeding TILA limits.

What does Section 8 of respa prohibit?

RESPA Section 8(a) prohibits the giving and accepting of kickbacks (e.g., cash or other “things of value” as defined in RESPA and Regulation X) pursuant to any agreement or understanding to refer settlement service business or business incident to a real estate settlement service in connection with those loans.

Who enforces respa?

Originally enforced by the U.S. Department of Housing & Urban Development (HUD), RESPA enforcement responsibilities were assumed by the Consumer Financial Protection Bureau (CFPB) when it was created in 2011.

Can a Texas Realtor pay a referral fee?

The short answer to this question is yes, real estate agents can pay referral fees to licensed persons.

Is a referral fee legal?

The California rule is one of a minority of states that permits a “pure referral fee,” i.e., California permits lawyers to be compensated for referring a matter to another lawyer without requiring the referring lawyer’s continued involvement in the matter.

What is fee splitting RESPA?

With respect to fee splitting, RESPA provides that no person shall give and no person shall accept any portion, split, or percentage of any charge made or received for the rendering of a real estate settlement service in connection with a transaction involving a federally related mortgage loan other than for services …

Which of the following forms of compensation is a violation of RESPA?

Which of the following forms of compensation is a violation of RESPA? The answer is a fee paid by a title company to an originator for referral of settlement services. RESPA requires any fees to be “earned.” Referral fees are considered a violation. You just studied 20 terms!

Which is an example of a kickback prohibited by RESPA?

Other forms of kickbacks illegal under RESPA include gifts, prizes and entries into raffles designed to reward agents for referring business, for example, to a title insurance company, surveyor or attorney.

What loans are exempt from RESPA?

When a loan is made to purchase vacant land, and none of the proceeds of the loan will be used to construct a covered residential structure, the loan is exempt from RESPA oversight. This is another case of the relative experience and knowledge of the participants in the transaction.

What is illegal under RESPA?

Section 8 of RESPA prohibits a person from giving or accepting any thing of value for referrals of settlement service business related to a federally related mortgage loan. It also prohibits a person from giving or accepting any part of a charge for services that are not performed.

Can a loan officer pay a referral fee?

Yes! Even in states where a license is required to broker commercial loans (California, Florida, Nevada, Arizona, etc.), you can legally pay a referral fee on a commercial mortgage loan, as long as the referring source does nothing more than call you with a name and phone number of a prospective borrower.

What is the maximum penalty for providing false information on a federally related loan?

The application states that knowingly making a false statement is punishable by a maximum of (1) five years’ imprisonment and/or a $250,000 fine under 18 U.S.C. §1001 (making false statements) and 18 U.S.C.

Does RESPA apply to HELOCs?

The TILA-RESPA rule applies to most closed-end consumer credit transactions secured by real property, but does not apply to: HELOCs; • Reverse mortgages; or • Chattel-dwelling loans, such as loans secured by a mobile home or by a dwelling that is not attached to real property (i.e., land).

What laws prohibit kickbacks?

§ 1024.14 Prohibition against kickbacks and unearned fees. Consumer Financial Protection Bureau.

What is the purpose of respa rules regarding escrow accounts?

Section 10 of the Real Estate Settlement Procedures Act (RESPA) provides protections for borrowers with escrow accounts. Specifically, it limits the amount of money that a lender may require the borrower to hold in an escrow account for paying taxes, hazard insurance and other charges related to the property.

Are markups legal under TILA?

Generally, yes. Although there are some exceptions, the large captive finance companies and the large banks all authorize dealers to markup customer interest rate, and split the profits.

What are the sections of respa?

- Loan Servicing Complaints (Section 6) …

- Kickbacks, Fee-Splitting, Unearned Fees (Section 8) …

- Seller Required Title Insurance (Section 9) …

- Limits on Escrow Accounts (Section 10) …

- RESPA Complaints and Enforcement.

Who is primarily liable for escrow violations?

In the majority of escrow cases, it is the depositary that incurs liability for a breach, usually due to their own misconduct. A depositary holding property in escrow for the parties owes a duty of care to both the grantor and the grantee. Failure to abide by the terms of the escrow agreement may result in a lawsuit.

What is the difference between RESPA and Tila?

TILA is the Truth in Lending Act and RESPA is the Real Estate Settlement Procedures Act.