What does FIN 48 stand for

Mia Kelly

Published Mar 15, 2026

In June, 2006 the Financial Accounting Standards Board issued Interpretation 48 of Financial Accounting Standard 109. This interpretation, known as “FIN 48”, is intended to eliminate inconsistency in accounting for uncertain tax positions in financial statements certified in accordance with U.S. GAAP.

What does Fin stand for in FIN 48?

FIN 48 stands for Financial Accounting Standards Board (“FASB”) No. 48, Accounting for Uncertainty in Income Taxes.

Is FIN 48 interest deductible?

Since the lawsuit’s settlement will not be deducted until payment is made (three to five years in the future), interest would accrue only after the first reporting period the tax return is due in which the deduction is taken on the tax return.

Is ASC 740 the same as FIN 48?

ASC 740, formerly known as FIN 48, offers guidance on uncertain tax positions. It is broad in scope and now applies to both nonprofit and for-profit entities.What is fin18?

FIN 18: Accounting for income taxes in interim periods.

What is FIN 48 Uncertain tax positions?

This interpretation, known as “FIN 48”, is intended to eliminate inconsistency in accounting for uncertain tax positions in financial statements certified in accordance with U.S. GAAP. FIN 48 mandates new rules for recognition, de-recognition, measurement, and disclosure of all tax positions.

Who is FIN 48?

FIN 48 is effective for fiscal years beginning after December 15, 2006, is applicable to all enterprises subject to US GAAP (including non-profit enterprises), and applies to all income tax positions accounted for in accordance with FASB Statement No. 109.

When did ASC 740 become effective?

740-10-55-140 In August 1991, a state amended its franchise tax statute to include a tax on income apportioned to the state based on the federal tax return. The new tax was effective January 1, 1992.What FAS 109?

FAS 109 Summary. This Statement establishes financial accounting and reporting standards for the effects of income taxes that result from an enterprise’s activities during the current and preceding years. It requires an asset and liability approach for financial accounting and reporting for income taxes.

Does ASC 740 apply to partnerships?The new partnership audit regulations will require partnerships conduct an ASC 740 review of their transactions.

Article first time published onWhat amount of tax benefit can be recognized for a tax position that meets a more-likely-than-not technical assessment?

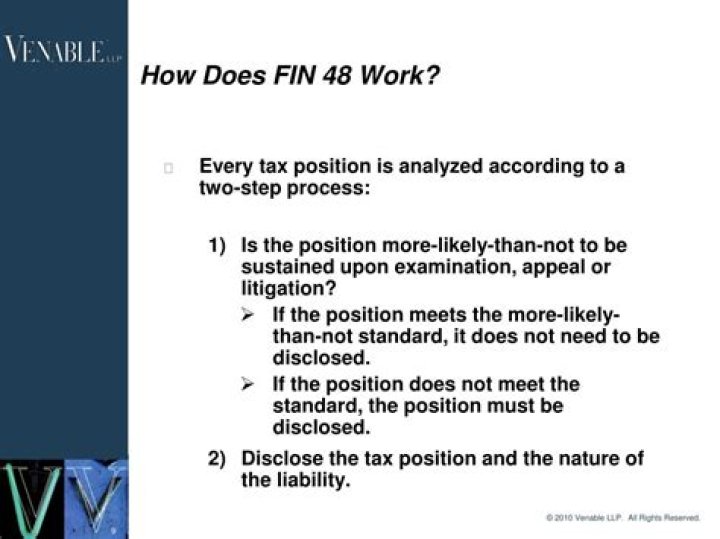

If a tax position meets the more-likely-than-not threshold, it should be measured based on the largest benefit that is more than 50 percent likely to be realized.

Who frequently disagrees with the position a company takes on its tax return?

The irs frequently disagrees with the position a companty takes on its tax return. Two step decision process: 1. A tax benefit may be reflected in the financial statements only if it is “more than likely not” that the company will be able to sustain the tax return position, based on its technical merits.

What are uncertain tax positions?

The IRS defines a UTP as a position taken on a tax return for which the corporation or a related party has recorded a reserve in its audited financial statements. A UTP also refers to instances in which a company hasn’t recorded a reserve for the position because it expects to litigate it.

What is apb23?

APB 23 (codified as FASB “ASC 740-10-25-3”) allows an exception to the general rule that a U.S. multinational company must accrue U.S. taxes on foreign earnings of its controlled non-U.S. subsidiaries. … As a result, the foreign earnings would not be subject to U.S. taxation via this assertion.

How is Aetr calculated?

The estimated annualized deferred effective tax rate is calculated by dividing the total deferred tax expense/(benefit) by the pre-tax net income after book adjustments.

What are discrete tax items?

A discrete item is accounted for: within the interim period that the event or transaction took place; and. at the applicable rate or rates (it is not a component of the estimated AETR).

What is a FAS 5?

FAS 5 is an underlying source of accounting guidance factoring into the calculation of the allowance for loan and lease losses (ALLL), and it applies to entities not yet subject to CECL. … Institutions using FAS 5 and FAS 114 need to implement CECL for 2023 or earlier, unless they are large SEC filers.

What replaced FAS 5?

5: Accounting for Contingencies (FAS 5), the original FASB pronouncement, superseded by the substantively same FASB Accounting Standards Codification (ASC) subtopic 450 -20, Contingencies: Loss Contingencies, is a principal source of guidance on accounting for impairment in a loan portfolio under GAAP.

What is valuation allowance?

A valuation allowance offsets part of a company’s deferred tax assets. It adjusts the value of the tax asset according to how much of the asset the company believes it will actually take advantage of. Valuation allowances should be disclosed on the balance sheet as an offset of the deferred tax asset.

What are the two steps used for reporting uncertain tax positions?

This Portfolio describes FASB’s two-step process for determining tax benefits that can be reported on the financial statements: (1) recognition—determine if the tax position meets the threshold test of “more likely than not” (MLTN) that the company will be able to sustain the tax return position, based solely on the …

What is a tax position?

tax position means an assumption underlying one or more aspects of a tax return, including whether or not— (a) an amount, transaction, event or item is taxable; (b) an amount or item is deductible or may be set-off; (c) a lower rate of tax than the maximum applicable to that class of taxpayer, transaction, event or …

What is ASC 740 tax?

Accounting for income taxes (ASC 740) is a set of income tax standards requiring public companies to analyze and disclose income tax risks. … Complying with ASC 740 is challenging for public companies due to the knowledge and experience needed to meet the significant tax and financial reporting requirements.

Did ASC 740 replace FAS 109?

This change will affect how financial statement preparers both research and reference GAAP. … Instead, references to GAAP will more closely resemble the Internal Revenue Code. Those in the tax field will no longer reference FAS 109 or FIN 48 but instead reference the topics: FASB ASC 740 (expenses).

How is deferred tax balance calculated?

How Deferred Tax Liability Works. It is calculated as the company’s anticipated tax rate times the difference between its taxable income and accounting earnings before taxes. Deferred tax liability is the amount of taxes a company has “underpaid” which will be made up in the future.

What is deferred tax asset with example?

One straightforward example of a deferred tax asset is the carryover of losses. If a business incurs a loss in a financial year, it usually is entitled to use that loss in order to lower its taxable income in the following years. 3 In that sense, the loss is an asset.

Which of the following best describes the scope of ASC 740?

Which of the following best describes the focus of ASC 740? ASC 740 takes an “asset and liability approach” that focuses on the balance sheet. … ASC 740 focuses on the balances in the deferred tax assets and liabilities on the balance sheet.

What is a controlling financial interest How did the FASB define this in FIN 46 R )?

A controlling financial interest is defined as an investment of 50% or more of the voting equity of another entity (or related group of entities).

Is the Oregon cat an income tax under ASC 740?

While Oregon does not deem the CAT to be an income tax, it appears to qualify as an income tax under ASC 740. This is because revenues are reduced by expenses in order to calculate the tax.

Are withholding taxes ASC 740?

If a franchise tax is partially based on income, it is subject to accounting in accordance with ASC 740. Withholding taxes that a reporting entity pays to the tax authority on behalf of its shareholders are also outside of the scope of ASC 740.

Is Texas franchise tax an income tax ASC 740?

ASC 740 implications Generally, Texas franchise tax is regarded as an income tax for income tax provision purposes under ASC 740. As previously stated, Texas regulations specifically provide that P.L. 86-272 protection does not apply to the franchise tax.

Is the Ohio Cat an income tax?

Ohio Commercial Activity Tax (CAT) is NOT an income tax or sales tax. It is a gross receipts tax imposed on the privilege of doing business in Ohio. … Combined filing can be required of businesses that have a common owner who owns or controls more than 50% of the value of each business.