How is goodwill calculated

Victoria Simmons

Published Apr 11, 2026

Goodwill is calculated by taking the purchase price of a company and subtracting the difference between the fair market value of the assets and liabilities. Companies are required to review the value of goodwill on their financial statements at least once a year and record any impairments.

What is hidden goodwill in retirement?

The amount paid to the retiring partner/deceased partner’s executor in excess of the amount actually due to them is hidden goodwill. Eg, If the amount due to a retiring partner/deceased partner’s executor id Rs. 20000 and the partners decide to pay him Rs. 25000 then ,hidden goodwill = 25000 – 20000 = Rs.

Why do we calculate goodwill?

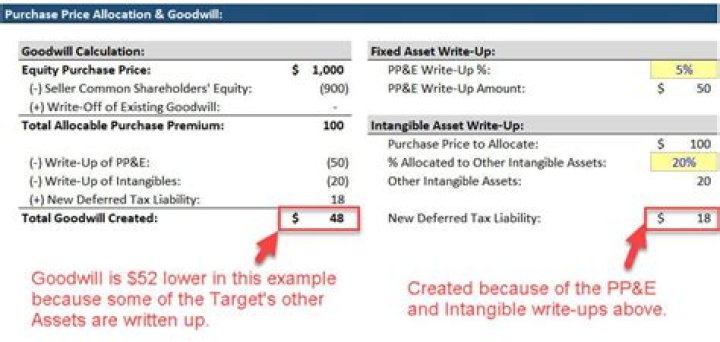

The need for determining goodwill often arises when one company buys another firm. Goodwill is calculated as the difference between the amount of consideration transferred from acquirer to acquiree and net identifiable assets acquired.

How is goodwill consolidation calculated?

IFRS 3 illustrates the calculation of consolidated goodwill at the date of acquisition as: Consideration paid by parent + non-controlling interest – fair value of the subsidiary’s net identifiable assets = consolidated goodwill.How do you calculate capital when goodwill is given?

- Goodwill = Normal Capital – Actual Capital Employed.

- # Normal Capital or Capitalized Average profits = Average Profits x (100/Normal Rate of Return)

- # Actual Capital Employed = Total Assets (excluding goodwill) – Outside Liabilities.

Why do we calculate gaining ratio?

2-Why is gaining ratio calculated? Ans: Gaining ratio is required to calculate the amount by which gaining partners’ capital accounts are to be debited to compensate for sacrificing partner. Gaining ratio is required to make adjustment of the present value of goodwill among partners.

How do you calculate sacrificing ratio?

- Sacrificing Ratio = Old Ratio – New Ratio.

- Gaining Ratio = New Ratio – Old Ratio.

- Q. Find a new profit sharing ratio for the following:

How is super profit goodwill calculated?

Calculate Super Profit as follows: Super Profit = Maintainable Average profits – Normal Profits. Calculate goodwill by multiplying super profit by the number of year’s purchase.How is goodwill calculated for a new partner?

Sometimes the value of goodwill is not given at the time of admission of a new partner. In such a situation, goodwill is calculated on the basis of net worth of the business. Hidden goodwill is the excess of desired total capital of the firm over the actual combined capital of all partners’.

How do you calculate goodwill amortization?Amortization Amount: The Amortization amount = Book Value of Assets. Assets Book Value Formula = Total Value of an Asset – Depreciation – Other Expenses Directly Related to it read more – Fair Value = 1300 – 1280 = 20.

Article first time published onHow do you calculate goodwill of a Class 12?

Goodwill is calculated by deducting the actual capital employed in business from the capitalised value of average profits. There will be no goodwill if the actual capital employed in the business exceeds or equals the capitalised value of the average profits.

What is raising goodwill?

Raise the goodwill at its value by crediting all the partners’ capital accounts (including that of the retired/ deceased partners) and then. Written off by debiting the remaining partners in their new profit sharing ratio and crediting the goodwill account with its full value.

When sacrificing ratio is equal to old ratio?

When a new partner is admitted, old partners have to sacrifice their profit share in favour of new partner and their old ratio gets reduced and whatever ratio left becomes a new ratio. Hence, as per equation: New Ratio = Old Ratio – Sacrifice Ratio. By interchanging the terms, Sacrifice Ratio = Old Ratio – New Ratio.

What is difference between sacrifice ratio and gaining ratio?

Sacrificing Ratio refers to the ratio in which the old partners of the firm give up or surrender their portion of profit in favor of the coming partner. Gaining Ratio implies the ratio in which the remaining partners of the firm, share the retiring partner’s profit share.

How do you calculate gain ratio?

- Gaining Ratio = New Ratio – Old Ratio.

- New Ratio = Old Ratio + Gain.

- Gaining Ratio = Retiring partner’s share x Acquisition Ratio.

- New Ratio = Old Ratio + Gaining Ratio.

What is the formula for calculating gaining ratio?

1. What is the Gaining Ratio? Ans. Gaining ratio can be explained as the difference between new profit sharing ratio and old profit sharing ratio.

How is profit sharing ratio calculated?

There are different scenarios when a business can have a new ratio. However, the calculation of the new profit sharing ratio in retirement is done simply by removing that retiring person’s share. In this scenario, the gaining ratio of the continuing members will be = retiring person’s share* Acquisition ratio.

When the amount of goodwill is paid privately?

This statement is True. Reason: When goodwill is paid privately to the partners, by a newly admitted person, then in such case no transaction takes place in the business and firm as such is not all benefited. Hence it is not recorded in the books of accounts.

When new partner does not take goodwill in cash?

When the new partner is not in a position to bring his share of goodwill in cash, then goodwill account is adjusted through the old Partners’ Capital Account.

How is goodwill paid privately by an incoming partner treated in the books of account?

Under this method, when the incoming partner brings his share of goodwill in cash, the existing partners share it in the sacrificing ratio. However, when the amount of goodwill is paid privately by the new partner to old partners privately in cash, no entry is passed in the books of the firm.

What is the ratio of sacrifice calculated for distribution of goodwill?

The ratio of sacrifice is calculated when the benefits of goodwill contributed by a new partner in cash is to be transferred to existing partners’ Capital/Current Account.

How do you value goodwill when selling a business?

What is Goodwill Worth: In a business sale, the overall value of goodwill is fairly straightforward; simply take the combined value of the business’ tangible assets (minus liabilities) and subtract that figure from the “fair market value” of the business.

Does goodwill need to be amortized?

Under GAAP (“book”) accounting, goodwill is not amortized but rather tested annually for impairment regardless of whether the acquisition is an asset/338 or stock sale.

How is goodwill treated in accounting?

How Goodwill Is Treated in the Financial Statements. … The $100,000 beyond the value of its other assets is accounted for under goodwill on the balance sheet. If the value of goodwill remains the same or increases, the amount entered remains unchanged. The amount can change, however, if the goodwill declines.

Can goodwill be Amortised?

In accounting, goodwill is accrued when an entity pays more for an asset than its fair value, based on the company’s brand, client base, or other factors. … Now, private companies can elect to amortize goodwill on a straight-line basis over 10 years, although this election is not required.

Which is not a method to calculate the goodwill?

Realisation method is not a method for valuation of goodwill. … (ii) Super Profit Method if the goodwill is valued at 3 years’ purchase of super profits.

How many methods of valuation of goodwill are there?

⇨ Capitalisation Method – Under this method, goodwill can be evaluated by two methods. Average Profits Method – In this process, goodwill is measured by subtracting the original capital applied from the capitalised amount of the average profits based on the average return rate.

How do you record goodwill in accounting?

Subtract the book value from the purchase price to calculate Goodwill. Goodwill is defined as the price paid in excess of the firm’s fair value. To calculate it, simply subtract the total asset market value amount from the purchase price; this amount is nearly always a positive number.

How does goodwill impairment affect income statement?

An impairment is recognized as a loss on the income statement and as a reduction in the goodwill account. The amount that should be recorded as a loss is the difference between the asset’s current fair market value and its carrying value or amount (i.e., the amount equal to the asset’s recorded cost).

How do you calculate old ratios?

When new partner purchases/gets/acquires/takes his share from old partners in a particular ratio then the new ratio of the old partners will be calculated by subtracting the proportion given to the new partner from the shares of old partners . Example: A and B are partners sharing profits in the ratio 3:2.

When goodwill is withdrawn by the partner which account is credited?

When goodwill is withdrawn by the partner Cash/Bank account is credited.