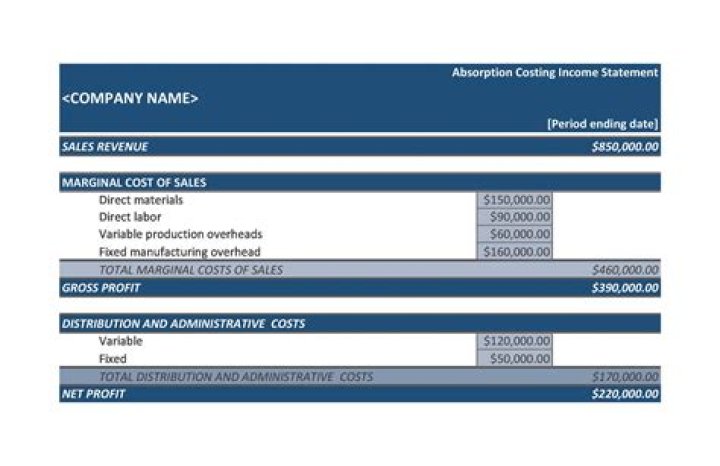

How do you create an absorption costing income statement

Emma Valentine

Published Mar 08, 2026

To find COGS, start with the dollar value of beginning inventory and add the cost of goods manufactured for the period. The resulting figure is goods available for sale. Subtract the ending inventory dollar value, and the result is cost of goods sold.

How do you do absorption costing on the income statement?

Under absorption costing, the cost per unit is direct materials, direct labor, variable overhead, and fixed overhead. In this case, the fixed overhead per unit is calculated by dividing total fixed overhead by the number of units produced (see absorption costing post for details).

Why would a company use absorption costing to prepare its income statements?

Using the absorption costing method will increase COGS and thus decrease gross profit per unit produced. This means companies will have a higher breakeven price on production per unit. … Furthermore, it means that companies will likely show a lower gross profit margin.

What is absorption costing with examples?

Absorption costing, sometimes called “full costing,” is a managerial accounting method for capturing all costs associated with manufacturing a particular product. The direct and indirect costs, such as direct materials, direct labor, rent, and insurance, are accounted for by using this method.How do you prepare a variable costing income statement?

- Contribution Margin =Revenue – Variable Production Expenses – Variable Selling and administrative expenses.

- Net profit or Loss = Contribution Margin – Fixed production expenses – Fixed Selling and administrative expenses.

What is absorption in financial accounting?

Absorption accounting is a method of accounting where all the costs of manufacturing, (including fixed, variable and mixed costs) are allocated to the produced units. … Another name for absorption accounting is full costing.

Which of the following would you find on an income statement prepared under absorption costing rules?

An income statement under absorption costing includes all of the following: Answer: Direct materials, direct labor, variable overhead, and fixed overhead.

How do you calculate absorption rate in accounting?

Based on this information, the rate of absorption is determined to be $40 per machine hour (calculated as $240,000 overhead costs divided by 6,000 machines hours). At the end of the current period, the cost accountant applies overhead costs to products using the $40/machine hour rate of absorption.When should Absorption Costing be used?

The uses are as follows: It is used in the determination of the profitable selling price of the products as it includes all the costs involved in the manufacturing of the product. It is used for inventory or stock valuation purposes.

How do you calculate under and over absorption?Under-absorption is set right by the plus rate while over-absorption is adjusted by minus rate. The supplementary rate may also be calculated as a percentage of the amount absorbed. Correction of overheads costs by a supplementary rate is nothing but recovering the overhead by actual rates.

Article first time published onWhy do companies use absorption costing for their internal reporting?

Some of the primary advantages of absorption costing are that it complies with generally accepted accounting principles (GAAP), recognizes all costs involved in production (including fixed costs), and more accurately tracks profit during an accounting period.

Which of the following is a reason why absorption costing income statements may be difficult to interpret?

A reason why absorption costing income statements are sometimes difficult to interpret is that: they shift portions of fixed manufacturing overhead from period to period according to changing levels of inventories.

What is difference between absorption costing and marginal costing?

Marginal costing is a method where the variable costs are considered as the product cost, and the fixed costs are considered as the costs of the period. Absorption costing, on the other hand, is a method that considers both fixed costs and variable costs as product costs.

What is a variable costing income statement used for?

Variable Costing is often used for internal decision-making. This is the costing method used for the contribution format income statement. • Variable costing classifies costs based on their behavior when the activity level changes: variable or fixed costs.

How are fixed manufacturing costs treated under absorption and variable costing?

Under absorption costing, fixed manufacturing overhead is treated as a product cost and hence is an asset until products are sold. Under variable costing, fixed manufacturing overhead is treated as a period cost and is immediately expensed on the income statement.

What are variable costs in income statement?

A variable cost is a corporate expense that changes in proportion to how much a company produces or sells. Variable costs increase or decrease depending on a company’s production or sales volume—they rise as production increases and fall as production decreases.

What costs are typically included in product costs under absorption costing?

Under absorption costing, companies treat all manufacturing costs, including both fixed and variable manufacturing costs, as product costs. Remember, total variable costs change proportionately with changes in total activity, while fixed costs do not change as activity levels change.

Does absorption costing treats all manufacturing costs as product costs?

2. Absorption Costing. Absorption costing treats all production costs as product costs, regardless of whether they are variable or fixed. Under absorption costing, a portion of fixed manufacturing overhead is allocated to each unit of product.

How do you reconcile variable and absorption costing?

Net income under absorption costing can be reconciled with net income under variable costing by (a) subtracting the manufacturing overheads carried forward (absorbed by closing inventories) and (b) adding the manufacturing overheads brought in (absorbed by opening inventories).

Why is absorption costing used for external reporting?

Absorption costing also account for the expenses of unsold products, this is important for external reporting as required by GAAP. This method achieves a better and higher net income estimation. This is because it helps to achieve less fluctuation in net profits.

What is absorption costing technique?

Absorption costing refers to a method of costing to account for all the costs of manufacturing. The management uses this method to absorb the costs incurred on a product. … Direct costs include materials, labour used in production. Indirect costs include factory rent, administration costs, compliance, and insurance.

What are the features of absorption costing?

The features associated with absorption costing are as follows: In the absorption costing a product, the cost is determined on the basis full cost, i.e., variable and fixed manufacturing cost. The cost of inventory will be higher in absorption costing as product cost includes fixed factory overhead.

How can the use of absorption costing result in overproduction?

In addition, absorption costing does allow for manipulation of income by managers through overproduction. Increasing production at year-end results in a higher net income than if the additional goods had not been produced, since increasing the number of units decreases the fixed cost per unit.

How do you calculate the rate of absorption in pharmacokinetics?

The absorption rate constant Ka is a value used in pharmacokinetics to describe the rate at which a drug enters into the system. It is expressed in units of time−1. The Ka is related to the absorption half-life (t1/2a) per the following equation: Ka = ln(2) / t1/2a.

What are the Formulae for method of absorption of overhead?

Machine Hour Rate Method: … The I.C.M.A., London, defines machine hour rate as “an actual or predetermined rate of cost apportionment or overhead absorption, which is calculated by dividing the cost apportioned or absorbed by the number of hours for which a machine is operated or expected to be operated”.

What is under absorption and over absorption in cost accounting?

The use of a predetermined rate may, therefore, result in under-absorption or over-absorption. When the amount absorbed is less than the actual overhead, there is under-absorption. Over absorption arises when the amount absorbed is more than the actual overhead.

Should operating income be calculated using variable costing or absorption costing?

The net operating income under variable costing systems is always higher than absorption costing system when inventory decreases during the period. When inventory increases, the fixed manufacturing overhead cost is deferred to inventory which reduces the current period’s total cost burden.

When absorption costing is used for external reporting variable costing can still be used for internal reporting purposes True False?

When absorption costing is used for external reporting, variable costing can still be used for internal reporting purposes. The use of absorption costing facilitates cost-volume-profit analysis. When absorption costing is used, management may be tempted to overproduce in a given period in order to increase net income.

Which of the following will usually be found on an income statement?

Once referred to as a profit-and-loss statement, an income statement typically includes revenue or sales, cost of goods sold, expenses, gross profits, taxes, net earnings and earnings before taxes.

Which cost would be included in product costs under both absorption costing and variable costing?

A cost that would be included in product costs under both absorption costing and variable costing is: supervisory salaries.

How marginal costing is an improvement over absorption costing?

The technique of Marginal Costing is a definite improvement over the technique of Absorption Costing. According to this technique, only the variable costs are consid- ered in calculating the cost of the product, while fixed costs are charged against the Page 5 26 Cost Management revenue of the period.