How are IFRS standards set

Emily Dawson

Published Mar 10, 2026

IFRS® Standards are set by the International Accounting Standards Board (Board) and are used primarily by publicly accountable companies—those listed on a stock exchange and by financial institutions, such as banks.

How IFRS standards are set?

IFRS® Standards are set by the International Accounting Standards Board (Board) and are used primarily by publicly accountable companies—those listed on a stock exchange and by financial institutions, such as banks.

Who develops IFRS standards?

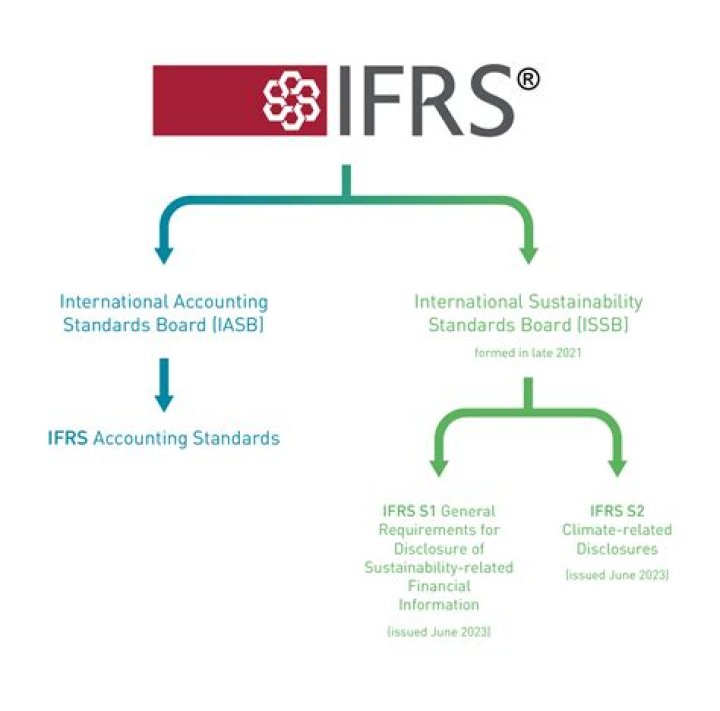

Our Standards are developed by our two standard-setting boards, the International Accounting Standards Board (IASB) and the newly created International Sustainability Standards Board (ISSB). The IASB sets IFRS Accounting Standards and the ISSB sets IFRS Sustainability Disclosure Standards.

What are the process for issuing IFRS?

- Research programme.

- Developing a proposal for publication.

- Redeliberations and finalisation.

- Post-implementation reviews.

How are standards set?

We cannot set a standard unless we decide what we want. We must set up a line of increase, a variable that operationalizes what we are looking for: This variable is usually brought to life by a test. Then it is the calibrations of the test’s items which define the line, and help us to decide how much is “enough”.

What are the 10 steps of the standard-setting process?

- Setting the agenda. …

- Planning the project. …

- Developing and publishing the discussion paper.

- Developing and publishing the exposure draft. …

- Developing and publishing the standard.

How are accounting standards set?

- First, the ASB will identify areas where the formulation of accounting standards may be needed.

- Then the ASB will constitute study groups and panels to discuss and study the topic at hand. …

- The ASB then carries out deliberations of the said draft of the standard.

How many standards are there in IFRS?

The following is the list of IFRS and IAS issued by the International Accounting Standard Board (IASB) in 2019. In 2019, there are 16 IFRS and 29 IAS.What are the 4 principles of IFRS?

IFRS requires that financial statements be prepared using four basic principles: clarity, relevance, reliability, and comparability.

What is IFRS need and procedure?IFRS specifies how businesses need to maintain and report their accounts. … IFRS covers a broad range of topics, including revenue recognition, income taxes, inventories, fixed assets, business combinations, foreign exchange rates, and the presentation of financial statements.

Article first time published onWhat is due process in standard-setting by IASB?

The due process comprises the requirements followed by the International Accounting Standards Board when setting IFRS Standards and developing the IFRS Taxonomy, and by the IFRS Interpretations Committee when working with the Board to support consistent application of those Standards.

How does accounting standards differ from accounting principles?

The main difference between Accounting Concepts and Accounting Principles is; Accounting concepts are the assumptions, guidelines, and postulates with which the accounting data is recorded whereas Accounting principles are the rules to be followed while reporting financial data.

What are the main objectives of IFRS?

- to develop, in the public interest, a single set of high quality, understandable, enforceable and globally accepted international financial reporting standards (IFRS Standards) based upon clearly articulated principles. …

- to promote the use and rigorous application of those standards;

What is a standard setting environment?

Environmental standards are typically set by government and can include prohibition of specific activities, mandating the frequency and methods of monitoring, and requiring permits for the use of land or water. …

What is the purpose of set standard?

Standards are set to publicly and internally hold the company work to be the best possible in its domain. Goals must connect with the standards. When a team is given an assignment to do work for a company client, the manager will have chosen the person or the team that is a good “fit” for this task.

How do you set relationships in standards?

The person must want me (have genuine interest in me, desire to spend significant time with me) The person must be honest, trustworthy, and faithful (the relationship is exclusive) I must feel safe with this person. The person must practice good self-care and not engage in unhealthy or destructive behaviors.

How are accounting standards enforced for compliance?

ADVERTISEMENTS: Compliance with accounting standards has been made mandatory. Sub-section (3A) to Section 211 (inserted by the Companies Amendment Act, 1999) requires that every profit and loss account and balance sheet shall comply with the accounting standards.

How can an accountant get benefit from setting accounting standards?

- 1] Attains Uniformity in Accounting. …

- 2] Improves Reliability of Financial Statements. …

- 3] Prevents Frauds and Accounting Manipulations. …

- 4] Assists Auditors. …

- 5] Comparability. …

- 6] Determining Managerial Accountability. …

- 1] Difficulty between Choosing Alternatives. …

- 2] Restricted Scope.

What do u mean by GAAP?

Generally Accepted Accounting Principles (GAAP or US GAAP) are a collection of commonly-followed accounting rules and standards for financial reporting. … The purpose of GAAP is to ensure that financial reporting is transparent and consistent from one organization to another.

Why IFRS is better than GAAP?

IFRS enables companies to portray a stronger balance sheet by allowing companies to report the fair market value of assets less accumulated depreciation. GAAP only allows the reporting of cost less accumulated depreciation.

What is difference between GAAP and IFRS?

The primary difference between the two systems is that GAAP is rules-based and IFRS is principles-based. … Consequently, the theoretical framework and principles of the IFRS leave more room for interpretation and may often require lengthy disclosures on financial statements.

Who sets US accounting standards?

Established in 1973, the Financial Accounting Standards Board (FASB) is the independent, private- sector, not-for-profit organization based in Norwalk, Connecticut, that establishes financial accounting and reporting standards for public and private companies and not-for-profit organizations that follow Generally …

What are the 10 accounting standards?

Accounting Standard (AS)Title of the ASRefer Note No.AS 10Accounting for Fixed AssetsAS 11The Effects of Changes in Foreign Exchange Rates10AS 12Accounting for Government GrantsAS 13Accounting for Investments

What are the 9 accounting standards?

Accounting Standard 9 (AS 9) is concerned with premises on the basis of which revenue is recognized in the statement of profit and loss of a business entity. This accounting standard deals with the recognition of revenue arising in the course of ordinary activities of the enterprise.

What are the new IFRS standards?

IFRS 17 establishes the principles for the recognition, measurement, presentation and disclosure of insurance contracts within the scope of the standard. … The IASB tentatively decided to defer the effective date of IFRS 17, Insurance Contracts to annual periods beginning on or after January 1, 2022.

How can I learn IFRS?

- Learn the basic structure of IFRS.

- Read the Framework.

- Get some knowledge about individual standards.

- Develop your knowledge and be up-to-date.

When did IASB assume its standard-setting responsibilities?

On April 1, 2001, the International Accounting Standards Board (IASB) assumed accounting standard-setting responsibilities from its predecessor body, the International Accounting Standards Committee.

What is the correct order for the process of issuing a new IFRS by the IASB?

- Introduction. …

- 1- Agenda Consultation. …

- 2- Research programme. …

- 3- Standard-setting programme. …

- 4- Maintenance programme.

What are the steps involved in due process?

Notice of the proposed action and the grounds asserted for it. Opportunity to present reasons why the proposed action should not be taken. The right to present evidence, including the right to call witnesses. The right to know opposing evidence.

What are the 3 basic accounting principles?

- Debit the receiver and credit the giver. …

- Debit what comes in and credit what goes out. …

- Debit expenses and losses, credit income and gains.

What are the two basic differences between principles and standards?

Principles are more broad, less defined, while standards are clear benchmarks to be used for assessing effectiveness (Gill, Kuwahara, & Wilce, 2016). Standards are also an attempt to operationalize values and re-establish norms, to make them consistent across the board, so that they reflect shared values.