Does recasting make sense

Victoria Simmons

Published Mar 02, 2026

If you have money saved up or receive a cash gift or inheritance, recasting your mortgage is an excellent way to invest in your home equity while keeping more of your income each month. Want lower monthly payments. By recasting your mortgage, you’ll reduce your loan principal and reduce your monthly payment amount.

Is it better to recast mortgage or pay down principal?

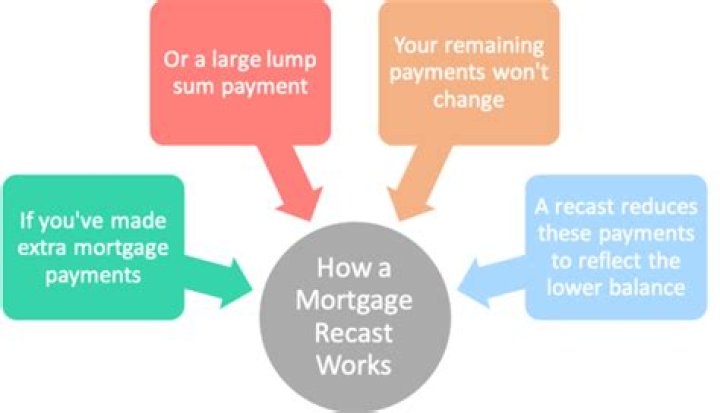

Recasting Advantages The biggest benefit of recasting is the lower monthly payment. A lower payment can be easier on your budget. The lower payment might free up cash that you can use for other financial goals, such as paying off other debts or saving for retirement.

How long do you have to wait to recast a mortgage?

Most lenders require proof of at least six months’ worth of payments before you can recast your mortgage. You won’t be able to change your loan terms. If current rates are lower, a recast doesn’t allow you to lower the rate or shorten the repayment term. You may lose some tax benefits.

Does recasting reduce interest?

Recasting your mortgage means that you can reduce your monthly payments, but the interest and terms remain the same. Or, you can refinance, which means replacing your current loan with a new loan that has better terms.What does recast your mortgage mean?

A mortgage recast is when a lender recalculates the monthly payments on your current loan based on the outstanding balance and remaining term. When you purchase a home, your lender calculates your mortgage payments based on the principal balance and the loan term. Every time you make a payment, your balance goes down.

Will my mortgage payments go down if I pay a lump sum?

Unless you recast your mortgage, the extra principal payment will reduce your interest expense over the life of the loan, but it won’t put extra cash in your pocket every month. …

Does Wells Fargo allow recast mortgages?

Wells Fargo, Bank of America, JPMorgan Chase and Quicken Loans offer mortgage recasts on some, though not all, of their loans. Recasts aren’t well known for a few reasons. Record-low interest rates in recent years made refinancing the go-to approach for borrowers looking to save on monthly payments.

Can you recast a conventional loan?

Mortgage recasting is only available on conventional loans, and is not an option for FHA, VA or USDA loans. … Once you apply for a mortgage recast, your lender will likely require you to make two consecutive payments (at your original payment amount) before it recasts the loan.What does Reamortize your loan mean?

Homeowners who are looking for a way to lower their monthly mortgage payments without changing their interest rate or loan terms should consider a mortgage recast. Recasting, or reamortizing, a mortgage can create both long-term and short-term savings.

Does recasting remove PMI?You can request to recast your mortgage and pay down on the principal, with the same interest rate. … This payment on the principal may be enough to get you below the 80 percent loan-to-value ratio and allow you to drop the PMI.

Article first time published onWhat is the purpose for recasting a loan when the borrower is in default?

A mortgage recasting, or loan recast, is when a borrower makes a large, lump-sum payment toward the principal balance of their mortgage and the lender, in turn, reamortizes the loan. This means that your loan is reduced to reflect the new balance.

What happens if I make a large payment on my mortgage?

Making a large early payment on your mortgage will reduce the amount of interest you pay on your loan. You’ll have a smaller loan balance, and interest is charged against your loan balance, so you’ll pay less.

How do I get rid of my PMI?

To remove PMI, or private mortgage insurance, you must have at least 20% equity in the home. You may ask the lender to cancel PMI when you have paid down the mortgage balance to 80% of the home’s original appraised value. When the balance drops to 78%, the mortgage servicer is required to eliminate PMI.

Is it wise to pay your mortgage off early?

Paying off your mortgage early can be a wise financial move. You’ll have more cash to play with each month once you’re no longer making payments, and you’ll save money in interest. … You may be better off focusing on other debt or investing the money instead.

What happens if you make 1 extra mortgage payment a year?

3. Make one extra mortgage payment each year. Making an extra mortgage payment each year could reduce the term of your loan significantly. … For example, by paying $975 each month on a $900 mortgage payment, you’ll have paid the equivalent of an extra payment by the end of the year.

How do I make a lump sum payment on my mortgage?

Make annual lump-sum payments In addition to your regular mortgage payment, use your prepayment privilege to make a lump-sum payment. It’s applied directly to your outstanding principal if you don’t owe any interest. Ask your lender how much you can prepay every year.

How can I pay off my 30 year mortgage in 10 years?

- Buy a Smaller Home.

- Make a Bigger Down Payment.

- Get Rid of High-Interest Debt First.

- Prioritize Your Mortgage Payments.

- Make a Bigger Payment Each Month.

- Put Windfalls Toward Your Principal.

- Earn Side Income.

- Refinance Your Mortgage.

Can I lower my mortgage interest rate without refinancing Wells Fargo?

The short answer is yes, though your options are very limited. If you’re facing financial turmoil, you may qualify for a mortgage rate reduction. But in most cases, you’ll either need to take another route to cut your mortgage costs or work toward getting a refinance approval.

Does paying more principal reduce interest?

Save on interest Since your interest is calculated on your remaining loan balance, making additional principal payments every month will significantly reduce your interest payments over the life of the loan. By paying more principal each month, you incrementally lower the principal balance and interest charged on it.

Why you shouldn't pay off your house early?

If you have no emergency fund because you put your extra money toward an early mortgage payoff, a single financial disaster could force you to take out costly loans. Or, if your mortgage hasn’t been paid off in full yet, an emergency could lead to foreclosure on your house if it means can’t pay the mortgage later.

Does Refinancing reset the amortization schedule?

Refinancing doesn’t reset the repayment term of your loan, but it does replace your current loan with a new loan. You may be able to choose from different offers for your new loan depending on your goals, including a longer or shorter repayment term.

Does Fannie Mae allow recasting?

Recasts are usually allowed on conventional and conforming Fannie Mae and Freddie Mac loans, though not FHA and VA loans. … A recast can’t be done within the first 90 days of a loan, but it can be done afterwards to reduce the principal and payments on the new loan. A loan recast doesn’t require an appraisal.

How can you avoid PMI without 20 down?

To sum up, when it comes to PMI, if you have less than 20% of the sales price or value of a home to use as a down payment, you have two basic options: Use a “stand-alone” first mortgage and pay PMI until the LTV of the mortgage reaches 78%, at which point the PMI can be eliminated. 1 Use a second mortgage.

How much should it cost to refinance my house?

Type of feeAmountApplication fee$75 to $500Origination feeUp to 1.5% of loan amountCredit report fee$30 to $50Home appraisal$300 to $400

What does PMI stand for?

Private mortgage insurance (PMI) is a type of insurance that may be required by your mortgage lender if your down payment is less than 20 percent of your home’s purchase price. PMI protects the lender against losses if you default on your mortgage.

Do extra payments automatically go to principal?

The interest is what you pay to borrow that money. If you make an extra payment, it may go toward any fees and interest first. … But if you designate an additional payment toward the loan as a principal-only payment, that money goes directly toward your principal — assuming the lender accepts principal-only payments.

What happens if I pay an extra $1000 a month on my mortgage?

Paying an extra $1,000 per month would save a homeowner a staggering $320,000 in interest and nearly cut the mortgage term in half. To be more precise, it’d shave nearly 12 and a half years off the loan term. The result is a home that is free and clear much faster, and tremendous savings that can rarely be beat.

Is it better to get a 30 year loan and pay it off in 15 years?

Refinancing from a 30-year, fixed-rate mortgage into a 15-year fixed-rate note can help you pay down your mortgage faster and save lots of money on interest, especially if rates have fallen since you bought your home. Shorter mortgages also tend to have lower interest rates, resulting in even more savings.

Can FHA PMI be removed?

Getting rid of PMI is fairly straightforward: Once you accrue 20 percent equity in your home, either by making payments to reach that level or by increasing your home’s value, you can request to have PMI removed.

Does Dave Ramsey own Churchill Mortgage?

If you’ve heard of Dave Ramsey, you might have come across Churchill Mortgage, which happens to be his mortgage lender of choice.

Does PMI go towards principal?

Private mortgage insurance does nothing for you This is a premium designed to protect the lender of the home loan, not you as a homeowner. Unlike the principal of your loan, your PMI payment doesn’t go into building equity in your home.